The taxation on property purchase, has become much simpler than it was before. With the roll-out of the Goods and Services Tax (GST), several taxes previously applicable on real estate purchase (VAT, service tax, etc.) have been subsumed under this single unified tax system.

The overall costs involved in buying a property are broadly divided into two components – the first being the one paid to the builder/seller and other, the statutory and legal costs, to the government. While the former roughly comprises 80-85 per cent of the overall property cost, the remaining 15-20 per cent goes as taxes to the government coffers. The taxes are not the same for under-construction and ready-to-move-in properties.

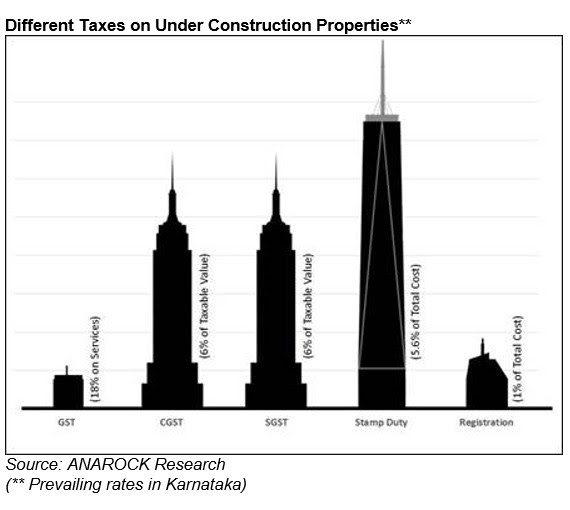

Taxes on under-construction properties

Statutory and legal costs for under-construction properties vary between 15-20 per cent, depending on the state in question and broadly include stamp duty, registration and GST.

- Stamp duty: Stamp duty is paid on the sale agreement, to render a property transaction legal and it varies from state to state.

For example, in Maharashtra, the stamp duty is five per cent (now proposed to be six per cent), while in Karnataka it is currently 5.6 per cent. As such, stamp duty accounts for between five to seven per cent to the total property acquisition cost. Interestingly, most states offer a rebate of one to two per cent to women, if a property is registered in their name.

- Registration charges: To register a sale agreement with a government-approved registration officer, buyers have to pay a registration fee of one per cent on the total cost of the property, at the district sub-registrar’s office.

- GST: Under the new tax-regime implemented in 2017, under-construction properties are currently taxed at 12 per cent on the base cost of a property. However, the GST Council is mulling reducing this rate, with many anticipating it to be reduced to either eight per cent or five per cent.

- TDS (tax deducted at source): TDS is charged at one per cent, for properties priced below Rs 50 lakhs. It is deducted by the buyer, at the time of payment to the seller. Thereafter, the builder needs to pay this amount to the central government online or via any authorised bank, within seven days from the end of the month in which such TDS was deducted.

See also: GST on real estate: How will it impact home buyers and the industry

Case study: Buying a home in Karnataka

Let us take these charges as applicable in Karnataka, to illustrate the calculations for an under-construction property with a super built-up area of 1,000 sq ft (carpet area of 780 sq ft) and priced at Rs 6,000 per sq ft. We will divide the overall cost into the total cost paid to the builder and to the state government.

Total cost paid to builder

1. Basic cost = Rs 60,00,000 (SBA* quoted rate, i.e., 1,000×6,000)

2. Cost of UDS/land value (One-third of basic cost, as per notification) = Rs 20,00,000

Thus, the total taxable value (basic cost less cost of USD/land value) = Rs 40,00,000

3. BESCOM, BWSSB and legal charges (calculated on per sq ft rate) = Rs 2,50,000

4. GST on water, electricity and other services (18 per cent on BESCOM, BWSSB and legal charges) = Rs 45,000

5. CGST (six per cent of taxable value) + SGST (six per cent of taxable value) = Rs 4,80,000*

Thus, the total cost paid to the builder = Rs 67,75,000 (basic cost + BESCOM/BWSSB/legal + GST + CGST + SGST)

Total cost paid to state government (during registration)

6. Stamp duty = Rs 3,79,400 (5.6 per cent of total cost to builder)

7. Registration charges = Rs 67,750 (One per cent of total cost to builder)

Grand total (Cost paid to builder + stamp duty and registration) = Rs 72,22,150

(* If the GST rate is brought down to eight per cent in the next Council meeting, the new GST cost paid to the government will be Rs 3,20,000 – a reduction of Rs 1,60,000)

Tax benefits of ready-to-move-in properties

One of the major attractions of ready-to-move-in properties, is that they are exempt from GST, provided that the project has been issued a completion certificate. Buyers of such properties need to pay only the stamp duty and registration charges as taxes, which comprise seven to eight per cent of the total property cost.

The seller quotes a lump-sum amount and the buyer also pays the government’s statutory charges during registration. Thus, ready-to-move-in properties offer a good value proposition for home buyers, who not only get to see the property they are buying but can also move in immediately and save on rentals.

Understandably, ANAROCK’s recent consumer sentiment survey indicates that buyer preferences are significantly skewed towards ready-to-move properties. More than 49 per cent of today’s property seekers prefer to buy ready properties, not only to save on costs but also to avoid risks such as delayed project delays and assorted unscrupulous builder activities.

Property tax

Another tax that a buyer needs to pay, after moving into his or her new home, is the annual property tax. The tax amount varies, not only from state to state, but also according to micro-markets in a city. In case there is an income generated by a property, that too is liable to be taxed. However, if the property is self-occupied, then, only the annual property tax applies.

Tax relief for affordable housing

In a major push to the affordable housing segment, the government has extended a GST benefit to its Credit-Linked Subsidy Scheme (CLSS) for EWS, LIG, MIG-I and MIG-II home buyers. Besides getting an interest subsidy, such buyers can also avail of a lower concessional GST rate of eight per cent.

In fact, to boost sales in this segment, the government has urged developers to refrain from charging any GST from home buyers in this critical segment, because the effective eight per cent GST rate in affordable housing can be adjusted against their input credit, should they opt for this.

How to save on property taxes

Tax deductions and exemptions which, if availed of appropriately, can go a long way in easing a home buyer’s overall financial burden.

Tax deductions on stamp duty and registration charges

While the government charges five to seven per cent of the property cost as stamp duty and registration taxes, one can claim tax deductions on these, under Section 80C of the Income Tax Act, 1961. Buyers can seek a maximum of Rs 1.5 lakhs as tax deduction, provided they fulfil certain conditions. For example, the taxes paid must be in the same year as that of claim, only fully-constructed properties are considered for this exemption and the property must be purchased for self-use and not as an investment.

Tax deductions on home loans

Buyers who avail of home loans, can claim tax deductions under Section 24, 80C and 80EE of the IT Act for repayment on both, the principal and interest amount, after fulfilling certain preconditions:

- Tax deductions on interest repayment: Under Section 24, a buyer can avail of deduction of a maximum of Rs two lakhs for the interest portion of the home loan for a self-occupied property. A property that is rented out has no upper limit for tax deduction claim.

- Tax deductions on principal repayment: Under Section 80C, one can claim a deduction of Rs 1.5 lakhs on repayment of the principal portion of the EMI paid during the year. However, the owner must not sell the property for at least five years after taking possession, or else, the deduction claimed earlier will be added back to owner’s taxable income in the year of sale.

- Additional benefit for first-time home buyers: Under section 80EE, first-time home buyers can claim an additional Rs 50,000 in deduction, provided the loan amount is Rs 35 lakhs or less and the property value does not exceed Rs 50 lakhs.

- Tax deductions on joint home loans: In case of a joint loan, each loan holder can claim a deduction of Rs two lakhs for interest paid and up to Rs 1.5 lakhs for the principal amount under Section 80C, provided they are the co-owners of the property purchased via the loan.

Saving tax on rental income

A property purchased for rental income is also subject to tax, but there are ways to save here, as well.

- Maintenance charges: An easy way to save tax on rental income, is to outright exclude maintenance charges from the rent received. One only needs to include the maintenance cost in the rental agreement.

- Municipal taxes: One can also claim municipality taxes like property tax, sewerage tax, etc., from the rental income, provided these charges are paid by the owner and not by the tenant.

- Additional tax benefit for jointly-owned property: In case of a jointly-owned property (usually, by a husband and wife) one can save on taxes quite effectively. For instance, if the wife is not working, the rental income can be divided in the proportion of ownership of the property and thus, one can save on taxes. This can also be beneficial in a scenario, wherein, both are working but are in different tax slabs.

- Basic deduction: One of the straightforward ways for owners to save more on a rented-out home, is to deduct an outright 30 per cent of the annual rental income for repair and maintenance of the property, irrespective of the actual expenditure incurred during the year.

(The writer is chairman, ANAROCK Property Consultants)