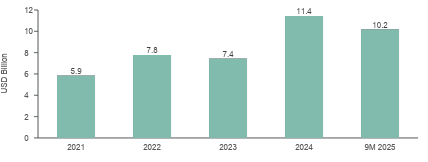

CBRE South Asia on October 10, 2025, published its latest report, ‘Market Monitor Q3 2025 – Investments’, highlighting that the total equity investments in the real estate sector jumped around 48% year-over-year (YoY) to $3.8 billion during the July-September quarter this year (Q3 2025). During Q3 2024, the inflows stood at $2.6 billion.

During Q3 2025, the inflows were primarily fuelled by capital deployment into land/development sites and built-up office and retail assets. In the first nine months this year (9M 2025), the equity investments increased by around 14% YoY to $10.2 billion from $8.9 billion in the same period last year.

Anshuman Magazine, chairman and CEO- India, South-East Asia, Middle East and Africa, CBRE, said, “The healthy inflow of domestic capital demonstrates the sector’s resilience and depth. India’s real estate sector is entering a phase of accelerated growth, driven by continued investor confidence. In the upcoming quarters, greenfield developments are likely to continue witnessing a robust momentum, with a healthy spread across residential, office, mixed-use, data centres, and I&L sectors”.

Gaurav Kumar, managing director, capital markets and land, CBRE India, added, “The investment landscape is becoming more diversified, with capital deployment into both built-up and development assets. In addition to global institutional investors, Indian sponsors accounted for a significant part of the total inflows. India’s ability to combine strong domestic capital with global institutional participation will remain a key differentiator in 2026 and beyond.”

Equity investments in the Indian real estate sector over the years (Source: CBRE Research)

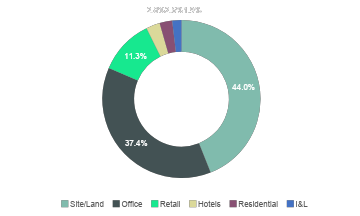

Asset-wise the growth was largely driven by sustained interest in land/development sites, along with robust activity in built-up asset acquisitions. Together, land/development sites and built-up office and retail assets accounted for more than 90% of the total capital inflows during Q3 2025.

Asset-wise share of equity investments in Q3 2025 (Source: CBRE Research)

Among major cities, Mumbai attracted the highest investments, accounting for a share of around 32%, followed by Pune (~18%) and Bengaluru (~16%). In the category of investors, developers remained the primary drivers of capital deployment, contributing approximately 45% of the total equity inflows, followed by institutional investors with a 33% share.

The report added that the investment activity in 2025 is expected to close on a strong note, primarily fuelled by capital deployment into built-up office and retail assets. Greenfield developments are likely to continue witnessing robust momentum in the upcoming quarters across residential, mixed-use, data centres and I&L sectors. For the office sector, the limited availability of investible core assets for acquisition indicate that opportunistic bets are likely to continue gaining traction.

| Got any questions or point of view on our article? We would love to hear from you. Write to our Editor-in-Chief Jhumur Ghosh at jhumur.ghosh1@housing.com |