While most home buyers avail of home loans to finance their property purchase, some buyers also choose to invest their own funds, to completely avoid the hassle and additional cost of financing, which is often more than the principal amount. However, with the Reserve Bank of India lowering key interest rates, banks too have started passing on the benefit to consumers. At the same time, fixed deposit rates have been lowered to around 5%-6%, which makes saving a less lucrative option for investors. So, what should be your ideal option, when buying a home – to opt for a home loan or use your own funds?

Is it better to take a home loan or pay cash?

Here’s how one can choose the better options:

- Calculate your interest income, i.e., the amount you have earned from FD interest, after paying taxes.

- Calculate the total interest on your home loan.

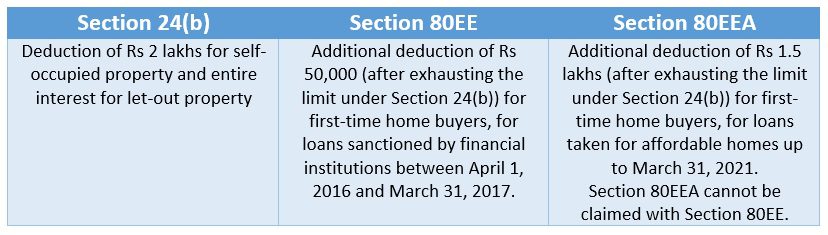

- Calculate the tax benefit that you can enjoy on your taxable income. Home buyers can enjoy tax benefits of up to Rs 3.5 lakhs per annum, on interest repayment and an additional Rs 1.5 lakhs on home loan principal and stamp duty registration charges.

- Calculate the net benefit of taking the loan, by evaluating the total tax benefit you would enjoy on interest payment during the entire tenure. You should also factor in the fact that in the initial years of repayment, the interest outflow will be higher and will reduce subsequently, as you repay a larger portion of the principal.

How to decide between home loan and own funds

To decide between home loan financing and using your own funds, let’s do some math. Suppose you opt for a loan of Rs 30 lakhs, at 7% interest for 10 years. Your total interest outgo will be Rs 11 lakhs. However, if you put the same amount in a deposit for 10 years at the current interest rate, your maturity amount will be Rs 47.1 lakhs. That means an interest income of Rs 17 lakhs, which is slightly more than the interest outgo if you apply for a home loan. In addition to this, if you opt for a home loan, you can enjoy price appreciation on your property, along with interest on your funds.

| Component | FD | Home loan |

| Principal | Rs 30 lakhs | Rs 30 lakhs |

| Tenure | 10 years | 10 years |

| Interest rate | 5.75% | 7% |

| Maturity amount | Rs 47.1 lakhs inflow | Rs 41.7 lakhs outgo |

See also: Rules for PF withdrawal for house purchase

Pros and cons of using own funds

| Pros | Cons |

| You do not have to pay any cost of financing to anyone. | You will not get any tax benefit. |

| No credit score check and lengthy paperwork. | Preferable, only when you have enough money to park in real estate. |

| No EMI burden | Your liquid funds will be invested in real estate, which may or may not lead to expected growth. |

| No need to worry about repo rate changes and fluctuations in interest rates. |

Check out: Information about Baroda Rajasthan Kshetriya gramin bank IFSC code

Pros and cons of home loan finance

| Pros | Cons |

| Home loan repayment is tax-saving. You get tax benefits on interest and principal repayment. | Interest component is much more than the borrowed sum. |

| It frees up your personal fund for portfolio diversification. | Formalities and documentation is a lengthy process. |

| Flexible tenure: Repayment is easy and highly customisable. | Long-term commitment and the property’s price appreciation may not meet your expectations. |

| Timely repayment of the home loan can boost your credit score. |

Thumb rule of home finance

- Apply for home loan when, Interest earned on deposit > Interest paid on home loan

- Use your own funds when, Interest earned on deposit < Interest paid on home loan

For example, if the home loan interest rate is around 7%-8%, applying for a home loan would be profitable only if the fixed deposit rates are more than the interest rate on the home loan. Apart from this, you should also consider the tax benefits that you will get, on interest and principal repayment.

See about: SBI IFSC code list

FAQs

When should I opt for a home loan?

Opt for a home loan when the interest earned on deposits is more than the interest paid on the home loan.

Should I use my own funds to buy a property?

Use your own funds to buy a property when the interest paid on the home loan is more than the interest earned through deposits.