It is a big financial decision to buy your first home. A hasty decision can easily ruin all your financial goals in life. So, it is always wise to take a planned step and proceed with caution. Most of the first home buyers take the help of home loans, which involves a long-term EMI repayment commitment.

What is EMI and how is it calculated?

Equated monthly instalment (EMI), is the amount that a borrower has to pay to the lender each month for a stipulated period, to repay the loan. Each EMI payment includes an amount towards repayment of the principal borrowed and the interest levied on the amount borrowed. The interest component in a home loan EMI is high during the initial repayment period, while the principal amount is relatively low. This proportion is reversed by the end of the home loan tenure. However, the EMI paid each month remains fixed, unless there is a change in interest rates.

How much EMI should you pay per month?

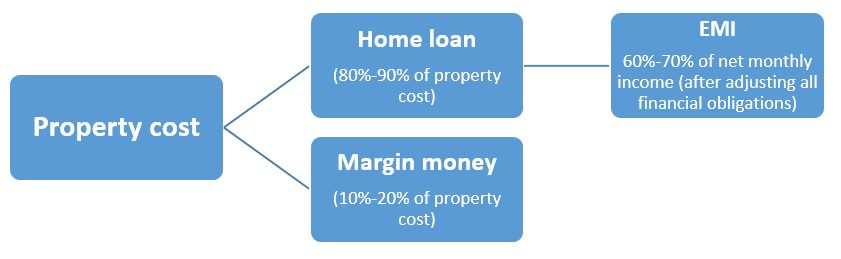

Early planning can help you to estimate how much loan you can afford and accordingly, you can start searching for a property. Usually, banks allow an EMI of up to 60% to 70% of net monthly income (after adjusting all financial obligations), while considering the loan application. For example, suppose your net monthly income is Rs 50,000 and your age is 30 years. Usually, the bank would allow an EMI up to 60% of 50,000 (i.e., Rs 30,000). If the rate of interest is 8% and you want to take the home loan for 30 years, then, you will be eligible to get a loan of up to Rs 68 lakhs, approximately. Considering this loan eligibility, you can start searching for a home that falls in your financial capacity.

Planning your home loan repayment can help you to save money towards the down payment, which amounts to around 10% to 20% of the value of the property. Early planning of home loans can allow you time to explore the terms and conditions of various lending institutions and banks and select the best lender. While the early planning of loans is crucial for first-time home buyers, it is equally important to repay your home loan on time. So, let us look at some ways to repay your home loan easily.

Should you prepay your home loan?

Bonus income can significantly reduce your home loan EMI obligation, or you can plan to repay your home loan early. Most salaried people get a bonus during the year. Instead of spending it completely, use it for prepayment of your home loan amount. Banks do not charge any penalty on prepayment of a floating rate-based home loan. Any lump-sum income from other sources, can also be used towards the payment of your home loan, to reduce your repayment obligation.

What is the best home loan tenure?

“For easy repayment, opt for the maximum permissible period, so that the EMI outgo will be easy. Also, at any point in time, if there is any shortage of income, you may not end up defaulting on the EMI. A few lenders even allow repayment period after retirement, at reduced EMIs, considering pension availability,” explains Deo Shankar Tripathi, MD and CEO of Aadhar Housing Finance. One can get a higher period of loan even after 60/70 years of age, by clubbing the income of one’s son/unmarried daughters or wife as co-borrowers.

How to increase your home loan eligibility

|

When should you switch a home loan?

Amit Sharma, CEO, Satin Housing Finance, points out that “There are various ways in which we can easily repay the loan. The first option, is by shifting to a lender who offers a low rate. Another option is to enhance the repayment capacity to increase the EMI and shorten the duration of the loan.” While switching from one lender to another, it is important to estimate the cost of switching and adjust it with the benefit that you would get due to the lower interest rate.

Home loan tax benefit and interest rate comparison

A home loan requires a very long-term repayment commitment. So, you must review your budget regularly, to use your income in the right way. Prioritise your expenses and focus on saving first and spending later, to repay your loan EMIs. A home loan comes with several tax benefits and it carries one of the lowest interest rates available in the market. So, before you plan to clear the home loan early, assess the impact of tax benefit that you would forgo. Compare the interest that you will save by early repayment, with the return that you expect to get by investing the same amount elsewhere and then, decide whether you should prepay the loan or not.

Why you should invest early for a home loan

According to experts, one should start investing early in one’s career, so that you can build a sufficient corpus, for buying your own home. If you have a big corpus while purchasing a home, then, it allows you a better cushion against liquidity crisis during the loan repayment period. It can help you to take a loan for a shorter period and avoid defaults on the loan repayment.

FAQs

What is margin money?

Banks generally provide up to 80%-90% of the property's cost as home loan, depending upon the credit profile of the borrower. The remaining 10%-20% of the cost, which the buyer had to pay from his own funds, is referred to as 'margin money'.

What is the minimum tenure of home loan?

Most banks and housing finance companies offer home loans for a minimum tenure of 5 years.

What is the maximum tenure of home loan?

Most banks and housing finance companies offer home loans for a maximum tenure of 5 years, or the number of remaining working years till retirement of the borrower.

Can I reduce my home loan tenure?

A home loan borrower can reduce the tenure of the loan, when the interest rate of the bank is reduced, or by switching the loan to another bank that offers lower interest, or by prepaying a part of the loan.

Is it advisable to prepay a home loan?

Prepaying a home loan, reduces the total interest paid to the lender. However, one should weigh the tax benefits available on the loan against the gains from investments that may need to be made in other avenues, before taking a decision to prepay a loan.