Before a bank approves a home loan application, it would examine the borrower’s repayment capacity by calculating the debt-to-income (DTI) ratio. Mostly calculated in percentage terms, the DTI ratio is obtained by dividing your net monthly income with your net monthly debt payments. Your debt payments could include payments towards credit card bills, education loans, auto loans, personal loans, etc.

DTI ratio formula

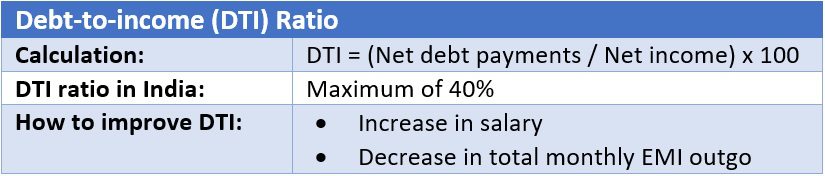

The formula used to calculate DTI ratio is:

DTI = Net debt payments / Net income

Since the result will show a decimal number, you have to multiply the result by 100, to get the DTI in percentage terms.

See also: What is an LTV ratio and how does it determine home loan eligibility?

Debt-to-income (DTI) ratio calculation

Suppose one Sunny Arora earns a monthly income of Rs 80,000. Of this, he pays Rs 25,000 as the EMI for his auto loan and Rs 15,000 as his education loan EMI. So, he is spending half of his income, i.e., Rs 40,000, every month in repaying his debt. Now if you divided his monthly income (i.e., Rs 80,000), with his monthly debt payments and then multiply the result (i.e., 0.5) by 100, the DTI ratio would be 50%.

Things home buyers should know about DTI ratio

Since a high DTI ratio could indicate an applicant’s inability to pay new EMIs, the higher the DTI ratio, lower are the chances of getting another loan. So, if the bank sees that a large part of your monthly income is spent on repaying your previous debt, they may not entertain your home loan request, even if you get a substantial salary every month. Conversely, the lower the DTI ratio, the higher your chances of getting a fresh loan.

A high DTI ratio will also be reflected in your credit report and a look at the same, would let the bank know, if you are likely to have any difficulty in repaying fresh loans. Also, note that one may have a good credit score in spite of a high DTI ratio, since a good credit score is generated by way of timely payment of your debts without any defaults. However, in case of a high DTI ratio, a good credit score may not be helpful in getting a new loan.

DTI ratio cap for Indian banks

In India, a DTI ratio of 40% is the highest that a borrower can have and can still get a new loan. Lenders would obviously prefer an applicant with a much less DTI ratio.

How to improve high DTI ratio?

The DTI ratio can be improved in two ways:

- An increase in your salary, or

- A decrease in your existing monthly payments.

While the first is possible in case you switch jobs or get a salary hike, the latter is possible if you get your existing loans refinanced, effectively lowering the monthly EMI payment while increasing the loan tenure.

If Arora, for example, lowers his education loan EMI to Rs 10,000 and his auto loan EMI to 20,000, his DTI ratio would be 37.5%. At this DTI ratio, lenders may be willing to approve another request for debt.

Also read: How to repay your home loan faster

Key notes about DTI ratio

- It is typically expressed in percentage terms.

- It is calculated on a monthly basis.

- Banks usually cap the DTI limit to 40%.

FAQs

What is the upper DTI ratio limit for Indian banks?

Banks in India will not approve your request for a fresh loan, if you use 40% of your net income to repay existing debts.

Can I get a home loan if 50% of my income is used in repaying other loans?

Banks may refuse your request in such a case.

What bills are included in debt to income ratio?

The lender will look at all your monthly debt payments to determine your debt-to-income ratio.