Record low interest rate on household savings, high unemployment rate and rising inflation levels, have added to the existing woes of home buyers in India, who are now battling with much higher debt-to-income (DTI) ratio than ever before. In spite of the advantages of lower interest rates in the aftermath of the Coronavirus pandemic, their DTI ratio has suddenly shot up beyond manageable levels.

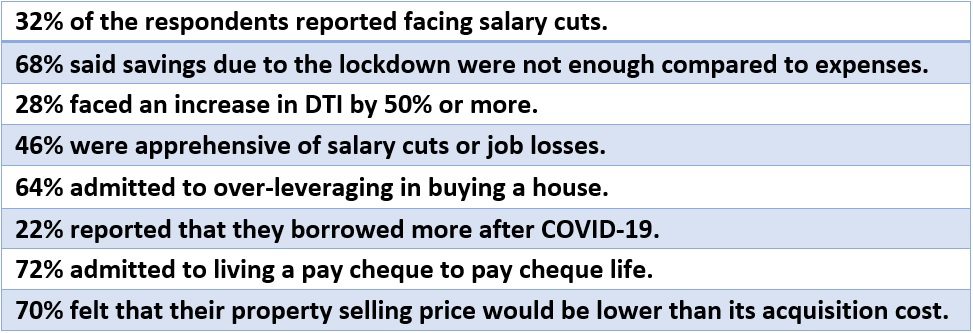

Following COVID-19, new buyers are playing safe and are careful to keep the LTV (loan-to-value) on the lower side. Nevertheless, the stress is definitely building up among existing buyers. According to an online poll by Track2Realty, nearly one-third of the participants (32% of respondents) reported that they had to take salary cuts after the pandemic, while 68% said that their savings were not enough to compensate for the salary cut.

Debt-to-income ratio worsens amid job loss, salary cuts

Take, for example, Naman Gupta, a communication professional. When he bought a house in the year 2017, his salary was Rs 1 lakh and the DTI ratio was well in balance, at 40%. Now that his salary has been cut by 30%, his DTI ratio has shot up to more than 50%, in spite of a lower interest rate. It is, hence, affecting his day-to-day expenses. “We all expect growth and not de-growth in jobs. When I had committed for an EMI of Rs 40,000, I was expecting a salary hike of 20%. It would have practically kept my DTI in the comfortable range of around 30%. However, I am now in a fix and with not much savings in hand, it will not be easy to keep serving the EMIs to retain the house for long,” says Gupta.

Gupta is not alone in facing a sudden increase in DTI. No less than 28% of Indian buyers in the survey reported that their DTI ratio increased to 50% or more. Even more worrisome, from the standpoint of existing home buyers, is the fact that after the second wave of COVID-19, 46% Indians are apprehensive of salary cuts or job losses in future.

A total of 64% buyers also admitted that they have over-leveraged their financial means and live with higher DTI ratio. Says S Ramaswamy, a software professional: “Yes, I do admit that I over-leveraged in my home purchase but then, I did not have the liberty of choice. In cities like Bengaluru, you either pay a hefty price to buy a house or keep paying a higher rent.” On the other hand, 22% of respondents reported having borrowed more, to sustain their livelihood and keep paying the housing EMI in the post-pandemic period.

See also: How to pay home loan EMIs in case of job loss due to the Coronavirus pandemic?

High home loan EMIs adding to the stress

When the debt-to-income ratio increases, the higher home loan EMIs may force borrowers to make compromises with one’s household budget. This is a situation that the average salaried class home loan borrower of today, is finding tricky to deal with. Home loan defaults are generally avoided in India and there are only a few cases of foreclosures in this part of the world. Home owners prefer to liquidate the property than default on EMIs, in case of financial distress.

However, there are clear indicators to suggest that financial distress is building up among Indians after salary cuts and job losses. Home loans, which comprise a major share of EMIs in India, are hence, under the scanner, after credit card defaults and gold loan distress sales.

- In May 2021, the cheque bounce rate for loan payments doubled to 21% from a year ago, as per data from Creditas Solutions.

- Credit card default also rose to 18% from 10% during the said period.

- Manappuram Finance auctioned gold worth about USD 55 million in the January-March quarter of 2021, compared to USD 1.1 million in the preceding three quarters combined.

- CRIF India that runs the Credit Bureau CRIF High Mark, says that overall home loan delinquencies have increased by 23 basis points (bps) to 2.49%, till December 2020.

Will the COVID-19 pandemic cause greater home loan defaults?

Data released by the Reserve Bank of India (RBI) show that India’s household financial savings rate dropped to 10.4% of the GDP in the July-September 2020 quarter, as compared to 21% in the preceding quarter. RBI data released in 2020 points out that household income, as indicated by the salary and wages bill of the country’s top listed companies, expanded at a compound annual growth rate (CAGR) of 4.3% against 17.7% CAGR growth in borrowing by households or individuals. So, it does not come as a surprise that 72% of respondents admitted that they were living a pay cheque-to-pay cheque life, after having bought a home.

Would this lead to foreclosures and distress sales in the housing market? Unfortunately, there is no clear answer to it, because 70% of buyers report the selling price in the secondary market today is much lower than their overall acquisition cost. “A distress sale at this point of time would be a huge loss. We would never be able to buy a house again,” says Prachi Desai in Mumbai.

What is the ideal DTI ratio?

The DTI ratio is a quantifying applied economic tool that divides the gross monthly income with the debt. Lenders use this, to determine if a potential borrower is eligible and capable of repaying the debt. Empirical evidence with housing loans, suggest that borrowers with a higher DTI ratio of above 50% are more likely to default in servicing the EMI of the home loan.

In most of the mature economies of the world, financial experts suggest a ‘28/36 rule’ as a comfortable level – one where your household expenses should not exceed 28% of its gross monthly income and the debt should not exceed more than 36%. A DTI ratio of 36%-43% indicates that the borrower has less room to handle any unforeseen expenses, while 50% or higher, is a clear red flag in other parts of the world. However, in India, it is a reality with a good number of buyers and now, with job losses and salary cuts, this is becoming unbearable for home buyers.

Any solution?

One should be more rational than emotional, vis-à-vis property purchase, to avoid future loan defaults and foreclosure, suggest experts. “There could be only two possible solutions when you are faced with a DTI ratio that is unmanageable. One, is to liquidate other savings and investments to pay upfront to the bank as much as possible and reduce the EMI. If you do not have any other savings, then, you should discuss it upfront with the bank and citing your changed financial situation, ask them for a loan restructuring for a longer tenure, to keep the EMI lower,” says Amitabh Sinha, an economic researcher.

FAQ

What is debt-to-income (DTI) ratio?

Debt-to-income (DTI) ratio refers to the percentage of one’s gross monthly income that is used to pay monthly debts.

What is the acceptable debt to income ratio?

An ideal DTI ratio is one where no more than 28% of the gross monthly income is spent on household expenses and no more than 36% is spent on debt.

(The writer is CEO, Track2Realty)