Those buying property market in the city have to pay stamp duty and registration charges in Hyderabad. After the stamp duty increase that came into effect from July 2022, stamp duty on property in Hyderabad is 7.5% of the property value as against 6% earlier. These charges include registration charges and transfer duty as well.

See also: All about WB registration

See also: Stamp duty and registration charges in Madhya Pradesh 2022

Stamp duty on other instruments in Hyderabad, Telangana 2024

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY | ||||||||

| 1 | ACKNOWLEDGMENT of a debt exceeding twenty rupees in mount or value written or signed by or on behalf of a debtor in order to supply evidence

of such debt in any book (other than a banker’s pass book) or on a separate piece of paper when such book or paper is left in the creditors possession: Provided that such acknowledgement does not contain any promise to pay the debt or an stipulation to pay interest or to deliver any goods or other property. |

Twenty paise | ||||||||

| 2 | ADMINISTRATION BOND including a bond given under section 291 or section 375 of the Indian Succession Act, 1925 ( central Act, 39 of 1925 ) or section 6 of the Government Savings

Bank Act, 1873 ( central Act, 5 of 1873) |

|||||||||

| a) | Where the amount does not 1, 000 | exceed Rs. | Three-fourths the duty as a Bond ( No: 13 ) for such

amount |

|||||||

| b) | in any other case | Thirty rupees | ||||||||

| 3 | ADOPTION DEED: that is to say any instrument ( other than a will) recording an adoption, or conferring or

purporting to confer an authority to adopt |

Thirty-five rupees | ||||||||

| 4 | AFFIDAVIT including an affirmation or declaration in the case of persons by law allowed affirm or declare instead of swearing.

EXEMPTION Affidavit or declaration in writing when made for the sole purpose of enabling any person to receive any pension or charitable allowances. |

Ten rupees | ||||||||

| 5 | AGREEMENT OR MEMORANDUM OF AN AGREEMENT :- | |||||||||

| (a) | If relating exchange: | to the | sale | of | a bill | of | One rupee | |||

| (b) | if relating to the sale of a Government Security or share in an incorporated company or other body corporate ; | Subject to an maximum of seventy- five rupees, fifty paise for every Rs. 10, 000 or part thereof, of the

value of the security or share . |

||||||||

| 6 | AGREEMENT OF MEMORANDUM OF

AN AGREEMENT:- not other wise provided for |

|||||||||

| (A) | Where the value | |||||||||

| i) | Does not exceed Rs. 5, 000/ – | Ten | Rupees | |||||||

| ii) | Exceeds Rs. 5, 000 /- but exceed Rs. 20, 000/- | does | not | Twenty Rupees | ||||||

| iii) | Exceeds Rs. 20, 000/- but exceed Rs. 50, 000/- | does | not | Fifty Rupees | ||||||

| iv) | Exceeds Rs. | 50, 000/- | One hundred rupees | |||||||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| (B) | If relating to construction of a house or building including a multi -unit house or building or unit of apartment / flat/ portion of multi-stored building or for development / sale of any other immovable property. | Five rupees for every one hundred rupees or part thereof on the market value or the estimated cost of the proposed construction / development of such property as the case may be, as mentioned in the agreement or the value arrived at in accordance with the schedule of rates prescribed by the Public Works Department Authorities which ever is

higher. |

|

| Note I : (a). Through the notification issued in G. O. Ms. No. 568, Revenue (Regn- I) Dept, Dt: 1. 4. 2008, the stamp duty in respect of instruments relating to Agreements or Memoranda of Agreements of sale/Constructions/ Development of immovable properties is reduced to 1% on the market value of the property as per the Basic value Guidelines or sale consideration shown in the document or estimated market value for land and complete construction made or to be made in accordance with schedule of rates approved by the C& IG, whichever is higher, which is not adjustable on subsequent sale deesds. This notification has been revoked through another notification issued in G. O. Ms. No. 1168 , Rev (Regn- I) Dept, Dt: 15. 9. 2010, w. e. f 20. 09. 2010.

Note II : (b). Through the notification issued in G. O. Ms. no. 1481, Revenue (Regn- I) Department, dt: 30. 11. 2007 , the stamp duty, in respect of instruments relating to Agreements or Memoran da of Agreements of Sale/ Construction/ Development of immovable properties combined with G. P. A clause, is reduced to 1% on sale consideration or market value of the property as per Basic value guidelines or the estimated market value for land and approved by the C& IG., whichever is higher is not adjustable on subsequent sale deeds. This notification has been partially rescinded through another notification issued in G. O. Ms. No. 1178, Rev( Regn- I) Department, Dt: 16. 9. 2010, w. e. f 20 . 9. 2010, in respect of Agree ments of Sale-cum-G. P. A. only. (c ). Through C& IG’s Circular Memo No. S 1/11217/2010, Dt: 22. 11. 2010, it has been clarified that Agreements or Memoranda of Agreements of Sale combined with G. P. A clause attract s 5% duty for the agreement clauses and 1% duty for the G. P. A clause. The duty paid for the agreement clauses has to be adjusted on subsequent sale deeds. The net effect of the above three reference is as follows. Instrument Rate of duty whether adjustable i) Agreement of sale 5 % Adjustable ii) ) Development Agreement 5 % Adjustable iii) Construction Agreement 5 % Adjustable iv) Agreement of sale- cum- G. P. A 6 % 5 % only is adjustable v) Development Agreement- cum- G. P. A 1 % Not adjustable vi) Construction Agreement- cum- G. P. A 1 % Not adjustable |

|||

| (c) | In any other Case | One hundred rupees | |

| 7 | AGREEMENT RELATING TO DEPOSIT OF TITLE DEEDS, PAWN OR PLEDGE,

or Hypothecation that is to say, any instrument evidencing an agreement relating to :- |

||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| (a) | The deposit of title- deeds or instrument constituting or being evidence of the title to any property whatever ( other than a marketable security), where such deposit has been made by way of Security for the repayment of money advanced or to be advanced by way of Loan or an existing

or future debt. |

0. 5% of the amount secured by such deeds, subject to maximum of Fifty Thousand Rupees. | |||

| (b) | the pawn, pledge or Hypothecation of movable property where such pawn, pledge or Hypothecation has been made by way of security for the repayment of money advanced or to be advanced by way of loan or an existing or future

debt:- |

||||

| (i) | If such loan or debt is repayable on demand or more than three months

from the date of the instrument evidencing the agreement: |

0. 5% of the amount secured, subject to a

maximum of Two Lakh Rupees. |

|||

| (ii) | If such loan or debt is re-payable not

more than three months from the date of such instrument |

Half the duty payable on a

loan or debt under sub- clause (i). |

|||

|

Explanation :- For the purpose of the clause( a) of this article, not withstanding anything contained in any judgement, decree or order of any court or order of any authority, and letter, note, memorandum or writing relating to the deposit of title deeds whether written or made either before or at the time when or after the deposit of title deeds is effected and whether it is in respect of the security for the first loan or any additional loan or loans taken subsequently, such letter, note, memorandum or writing shall, in the absence of any separate agreement or memorandum of agreement relating to deposit of such t itle deeds, be deemed to be an instrument, evidencing an agreement relating to the deposit of t itle deeds. Exemption :- 1. . Letter of hypothecation accompanying a bi l l of exchange duly stamped. 2 . Unattested instrument of pawn or pledge of, — (a) ) Farm equipment and Tractors; (b) ) Any goods for a loan secured upto one lakh rupees. |

|||||

| 8 | APPOINTMENT IN EXECUTION OF

A POWER, whether of trustees or of property, movable or immovable, where made by any writing not being a will |

Sixty rupees. | |||

| 9 | APPRAISEMENT OR VALUATION

made otherwise than under an order of the court in the course of a suit— |

||||

| a) | Where the amount does not exceed Rs. 1, 000 /- | The same duty as Bottomry

Bond (No. 14) for such amount. |

|||

| b) | In any other case, | Thirty rupees | |||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| 10 | APPRENTICES- SHIP DEED,

Including every writing relating to the service or tuition of any apprentice, clerk or servant placed with any master to learn any profession, trade or employment.

EXEMPTION Instruments of apprenticeship executed by a Magistrate under the Apprentice Act 1961(central Act 52 of 1961 ) or by which a person is apprenticed by or at the charge of any public charity. |

Fifteen rupees | ||||||||

| 11 | ARTICLES OF ASSOCIATION OF COMPANY | |||||||||

| (i) | Where

Capital |

the | company | has | no | Share | One Thousand Rupees | |||

| (ii) | Where the Company has authorised | 0. 15% of such authorised | ||||||||

| Share Capital or increased Share | Share Capital subject to a | |||||||||

| Capital. | minimum of One Thousand | |||||||||

| Rupees and a maximum of | ||||||||||

| Five Lakh Rupees. | ||||||||||

| 12 | AWARD, that is to say, any decision in writing by an arbitrator or umpire, not being an award directing a partition on reference

made other wise than by an order of the Court in the course of a suit – |

|||||||||

| a) | Where the amount or value of the property to which the award relates,

as setforth in such award, does not exceed 1000. |

The same duty as Bottomry Bond (No. 14) for such amount. | ||||||||

| b) | If it exceeds Rs. 1000 but does not exceeds Rs. 5000 .

And for every additional Rs. 1000 or part there of in excess of Rs. 5000; |

Fifty rupees | ||||||||

|

Two rupees |

subject to a |

|||||||||

| maximum of | two hundred | |||||||||

| rupees. | ||||||||||

| 13 | BOND [as defined by section 2( 5),] not being a debenture and not being otherwise provided for by this Act or by the Andhra Pradesh Court Fees

and Suits Valuation Act, 1956( Andhra Pradesh Act VII of 1956 ) |

|||||||||

| a) | Where the amount or value secured does not exceeds Rs. 1000. | Three rupees for every one

hundred rupees or part thereof. |

||||||||

| b) | Where it exceeds Rs. 1, 000/ -.

EXEMPTION Bond, when executed by an person for the purpose of guaranteeing that the local income derived from private subscriptions to a charitable dispensary or hospital or any other object of public utility, shall not be less than a specified sum per mensem. |

The same duty as under clause ( a) for the f irs Rs. 1000 and for every Rs 5, 00 or part thereof in excess of Rs. 1, 000/- fifteen rupees | ||||||||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| 14 | BOTTOMRY BOND , that is to say, any instrument where by the master of a sea-going ship borrows money, on the security of the ship to enable him to preserve the ship or

prosecute her voyage : – |

|||||

| a) | Where amount or value does not exceeds Rs. 1, 000; | secured | Three rupees for every one hundred rupees or part

thereof; |

|||

| b) | Where it exceeds Rs. 1, 000 | The same duty as under clause ( a) for the f i rst Rs. 1000 and for every Rs. 500

or part thereof in excess of Rs. 1, 000 /- fifteen rupees. |

||||

| 15 | CANCELLATION- INSTRUMENT of

(including any instrument by which any instrument previously executed is cancelled), if attested and not otherwise provided for |

Thirty | rupees | |||

| 16 | CERTIFICATE OF SALE –

( in respect of each property put up as separate lot and sold, granted to the purchaser of any property sold by public action by a Civil or Revenue Court or the Collector or other Revenue Officer. |

|||||

| a) | Where the purchase money does not exceed Rs. 10 | One rupees | ||||

| b) | Where the purchase money exceeds Rs. 10/- but does not exceeds Rs.

25/-. |

One rupees fifty paise. | ||||

| c) | In any other case | The same duty as conveyance (No: 20 ) for a consideration or market value equal to the amount of the purchase money

only. |

||||

| 17 | CERTIFICATE OR OTHER

DOCUMENT evidencing the right or title of the holder thereof, or any other person, either to any shares, scrip or stock in or of any incorporated Company, or other body corporate or become proprietor of shares, scrip or stock in or of any such company or body. |

Thirty paise | ||||

| 18 | 1) | CHARTER PARTY, that is to say, any instrument ( except an agreement for the hire or a tug -steamer), whereby a vessel or some specified principal part thereof is let for the specified purposes of the charter,

whether it includes a penalty clause or not. |

Five | rupees | ||

| 2) | A CHIT AGREEMENT, that is to say an agreement relating to a chit as defined in clause (2 ) of section 2 of the Andhra Pradesh Chit Funds Act, 1971, i f either such agreement is executed or the chit is conducted in

the State of Andhra Pradesh where the value of the Chit:- |

|||||

| (i) | Does not exceed rupees one lakh | Ten Rupees. | ||||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| (ii) | Exceeds rupees one lakh | Fifty Rupees | ||

| 19 | COMPOSITION DEED, that is to say any instrument executed by a debtor where by he conveys his property for the benefit of his creditor, or where by payment of a composition or dividend on their debts is secured to the creditors, or whereby provision is made for the continuance of the debtor’s business, under the supervision of inspectors or under letters of

license, for the benefit of his creditors; |

Thirty-five rupees. | ||

| 20 | CONVEYANCE as defined by section 2(10), not being a sale, charged

under (No. 47 -A) or a transfer charged or exempted under No. 53. |

|||

| a) | Where the amount or value of the consideration for such conveyance as set- forth therein of or the market value of the property which is the subject matter of the conveyance whichever is higher does not exceed Rs. 50; | Two rupees fifty paise | ||

| b) | Where it exceeds Rs. 50 but does not exceed Rs. 1, 000 | Five rupees for every one hundred rupees or part

thereof. |

||

| c) | Where it exceeds Rs. 1, 000

Provided that where an agreement to sell immovable property is stamped with the advalorem stamp required for a conveyance on sale under Article 47- A and a conveyance on sale in pursuance of such agreement is subsequently executed, the duty on such conveyance on sale shall be the duty payable under the article less the duty already paid under article 47- A subject to minimum of five rupees. |

The same duty as under clause (b) for the First Rs. 1000, and for every Rs. 500 or part thereof in excess of Rs. 1000/- Twenty-five rupees. | ||

| d) | Conveyance, so far as it related to amalgamation or merger of companies under the order of High Court under section 394 of the Companies Act, 1956 | Two rupees for every one hundred rupees or part thereof the market value of the property, which is

the subject matter of such conveyance. |

||

| Explanation :- For the purpose of the clause(d) the market value of the property shall be deemed to the amount of total value of the shares issued or allotted by

the transferee company, either in exchange or otherwise, and the amount of consideration, i f any, paid for s uch amalgamation or merger. |

||||

| 21 | COPY OR EXTRACT , certified to be a true copy or extract by or by order of any public officer and not chargeable under the law for the

time being in force relating to court fees— |

|||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| i) | If the original was not chargeable with duty , which i t was chargeable does not exceed two rupees fifty

paise |

Ten rupees | |

| ii) | In any other case.

EXEMPTION a) Copy of any paper which a public officer is expressly required by law to make of furnish for record in any public office or for any public purpose.

b) Copy of or extract from, any register relating to births, baptisms, namings, dedications, marriages, divorces, death or burials. |

Twenty rupees | |

| 22 | COUNTERPART OR DUPLICATE of

any instrument, chargeable with duty and in respect of which the proper duty has been paid become proprietor of share, scrip or stock in or of any such company or body. |

||

| a) | If the duty with which the original instrument is chargeable does not

exceed ten rupees |

The same duty as is payable on the original. | |

| b) | In any other case. | Twenty rupees | |

| 23 | CUSTOMS BOND- | ||

| a) | Where the amount does not exceed Rs. 1000: | The same duty as a Bottomry Bond ( No: 14 ) for such amount. | |

| b) | In any other case | Thirty rupees | |

| 24 | DELIVERY ORDER in respect of goods that is to say, any instrument entitling any person therein named, or his assigns or the holder thereof to the delivery of any goods lying in any dock or port or any warehouse in which goods are stored or deposited or rent or hire, or upto any wharf, such instrument, being signed by or on behalf of the owner, of such goods upon the sale or transfer of the property therein, when such goods exceed in value twenty

rupees. |

Twenty rupees. | |

| 25 | DIVORCE: – instrument of that is to say any instrument by which any

person effects the dissolution o his marriage. |

Five rupees |

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| 26 | ENTRY AS AN ADVOCATE on to roil of the Bar Council of Andhra Pradesh under the Advocate Act, 1961.

EXEMPTION

Entry as an Advocate on the roll of the Bar Council of Andhra Pradesh when he has been previously enrolled as a Vakil in Andhra Pradesh High Court or as an Advocate or Vakil in any other High Court |

Two hundred and fifty rupees or if previously enrolled as an Attorney in any High Court, one hundred twenty five rupees. | ||

| 27 | EXCHANGE OR PROPERTY

instrument of |

The same duty a a conveyance ( no 20) for a consideration or market value equal to the market value of the property of greater value, which is the subject matter of

exchange. |

||

| 28 | FURTHER CHARGE- instrument of that is to say any instrument imposing a further charge on

mortgaged property — |

|||

| a) | When the original mortgage is one of the descriptions referred to in clause ( a) of Article 35 ( that is , with procession) | The same duty a Conveyance ( No : 20) for a consideration or market value equal to the amount of the further charge secured by such

instrument. |

||

| b) | When such mortgagee is one of the discretion referred to in clause (b)

of Article 35 ( that is , without possession): |

|||

| i) | If at the time of execution of the instrument of further charge possession of the property is given or agreed to be given under such instrument: | The same duty as a conveyance (No 20), for consideration or market value equal to the total amount of the charge including the original mortgage and any further charge already made), Less the duty already paid on such original mortgage and

further charge. |

||

| ii) | If possession is not so give | The same duty as a Bottomry Bond ( No: 14) for the amount of the

further charge secured by such instrument |

||

| 29 | GIFT – Instrument of , not being a settlement ( No: 49) or will or Transfer ( No: 53 ) | The same duty a conveyance (No: 20 ) for a consideration or market value, of the property which is the subject matter

of gift. |

||

| 30 | INDEMNITY BOND | The same duty as a security Bond ( No: 48)

for the same amount |

||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| 31 | LEASE, including an under lease or sub- lease and any agreement to let or sublet or any renewal of lease:- | |||

| a) | Whereby such lease the rent is f ixed and no premium is paid or delivered | |||

| i) | Where the lease purports to be for a term of less than one year; | 0. 4% on the whole amount payable on such lease. | ||

| ii) | Where the lease purports to be for a term of not less than one year but

not more than five years. |

0. 4% on the total rent payable on such lease. | ||

| iii) | Where the lease purports to be for a term exceeding five years but not

exceeding ten years |

0. 4% on the total rent payable on such lease. | ||

| iv) | Where the lease purport s to be for

a term exceeding ten years, but not exceeding twenty years: |

0. 6% on the total rent payable on such lease. | ||

| v) | Where the lease purports to be for a

term exceeding twenty years, but not exceeding thirty years |

0. 8% on the total rent payable on such lease. | ||

| vi)a | Where the lease purports to be for a period in excess of thirty years or in perpetuity or does not purport to be for a definite period. | 5% on the value of property under lease as declared by the party or 0. 8% on the total rent

payable on such lease, whichever is higher. |

||

| vi)b | Where the lease is granted for a fine or premium or for money advanced

or to be advanced and where no rent is reserved. |

5% on the fine or premium or money advance or to be advanced as set forth in

the lease. |

||

| vi)c | Where the lease is granted for a fine or premium or for money advanced in addition to rent reserved. | 5% on such f ine or premium or money advanced in addition to the duty which would have been payable on such lease, if no f ine or

premium or advance had to be paid or delivered. |

||

| d | Where the lessee undertakes to effect improvements in the leased property and agrees to make the same to the lessor at the t ime of termination of lease failing under clauses ( a),(b) or ( c ); | 5% on the value of the improvements

contemplated to be made by the Lessee as set forth in the deed in addition to the duty chargeable under clauses ( a) or (b) or (c ) |

||

| Note: Through the notification issued in G. O. Ms. No. 408 ,

Revenue (Regn-I) Department, Dt: 11. 5 . 2010, the stamp duty on lease deeds is reduced, w. e. f 14. 5. 2010 as mentioned above. |

||||

| Exemption :- Lease, executed in case of a cultivator and for the purpose of cultivation (including a lease of trees for the prod uction of food or drink) without the payment or delivery of any f ine or premium, when a definite term is expressed and such term does not exceed one year, or when the average annual rent reserved does not exceed one thousand rupees.

Explanation :- When a lessee undertakes to pay any recurring charge, such as Government revenue, the landlord’s share of cesses, or the owner’ s share of municipal rates or taxes, which is by law recoverable from the lessor, the amount so agreed to be paid by the lessee shall be deemed to be part of the rent. |

||||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| vi)d | Where the lessee undertakes to effect improvement in the leased property and agrees to make the same to the lessor at the time of termination of lease falling under clauses( a),(b) or ( c); | Five percent on the value of the improvements contemplated to be made by the lessee as setforth in the deed in addition to the duty chargeable by the

clauses( a),(b) or ( c). |

||

| 32 | LETTER OF ALLOTMENT OF

SHARES in any company or proposed company, or in respect of any loan to be raised by any company or proposed company |

Thirty paise | ||

| 33 | LICENSEE of immovable or movable property , that is to say l icence granted by owner or authority for rent or fee or by whatev er name it

is called :- |

|||

| (a) | Whereby such licence granted for rent or fee or by what ever name it is called :- | |||

| (i) | Where the licence purports to be for a term of less than one year | Two rupees for every one hundred rupees or part thereof for the first Rs. 1000/- and for every Rs. 500/- or part thereof in excess of Rs 1, 000/- ten rupees, for the whole amount payable , or deliverable under such

licence; |

||

| (ii) | where the l icence purports to be for a term of not less that one year but not more than five years | Two rupees for every one hundred rupees or part thereof for the first Rs. 1000/- and for every Rs. 500/- or part thereof in excess of Rs 1, 000/- ten rupees, for the amount or value of the average annual rent or fee or by whatever name it is called

, |

||

| (iii) | Where the l icence purports to be for a term of not less than five years gut not exceeding ten years ; | Five percent on the amount or value of one and half time of the average annual rent or fee

or by what ever name it is called ; |

||

| (b) | Where the licence is granted for a lumpsum amount advanced in

addition to rent or fee or by what ever name it is called |

Five percent on the lumpsum amount as setforth in the l icence. | ||

| (c) | Where the l icence is granted for a lumpsum amount advanced in addition to rent or fee or by whatever name it is called; | Five percent on the lumpsum amount advanced as setforth in the licence in addition to the duty which would have been payable on such licence i f no lumpsum

amount advanced had been paid or delivered |

||

| 34 | MEMORANDUM OF ASSOCIATION OF A COMPANY :- | |||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| a) | If accompanied by Articles of Association under Section 26 of the Companies Act, 1956 ( central Act

of 1956 ) |

Five | hundred rupees | ||

| b) | If not so accompanied | The same duty as under article 11, according to the share capital of the

company |

|||

| 35 | MORTGAGE DEED not being an agreement relating to Deposit of Title Deeds, Pawn or Pledge (No: 7), Bottomry Bond ( no 14 ), Mortgage of a crop (No: 36 ) Respondentia Bond (No: 47 ) or

Security Bond ( No: 48). |

||||

| a) | When possession of the property or any part of the property comprised in such deed is given by the mortgage or agreed to be given; | The same duty as a Conveyance ( No: 20 ) for a consideration or market value equal to the amount

secured by such deed. |

|||

| b) | When possession is not given agreed to be given as aforesaid; | or | The same duty as a Bottomry Bond (No: 14) for

the amount secured by such deed. |

||

| Note: Through the notification issued in G. O. Ms. No. 409, Revenue (Regn- I) Department, dt: 11. 5. 2010, the duty chargeable on simple mortgages under Article 35(b) is reduced from 3% to 0. 5% of the amount secured by such deeds,

e. e. f 14. 5. 2010 |

|||||

|

EXPLANATION A mortgagor who gives or has given to the mortgagee a power of attorney to collect rents, or has given to the mortgagee a lease, of the property mortgaged or part thereof, is deemed to give possession thereof within the meaning of this article. |

|||||

| c) | When a collateral or auxiliary or additional or substituted security , by way of further assurance for the above mentioned purpose where the principal or primary security is duly

stamped. |

||||

| For every sum secured exceeding Rs. 1000/- | not | Three rupees | |||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| and for every Rs. 100/- or part thereof secured in excess or Rs. 1000/-

EXEMPTION Instruments executed by persons taking advances under the Land Improvement Loans Act, 1883 (Central Act 19 of 1883) or the Agriculturists Loan Acts 1884, or by the their sureties as security for the repayment of such advances . |

Three rupees | |||

| 36 | Mortgage of a Crop, including any instrument evidencing an agreement to secure the repayment of a loan made upon any mortgage of a crop; whether the crop is or is not in

existence at the mortgage |

|||

| a) | When the loan is repayable not more than three months from the

date of the instrument— |

|||

| For every sum secured not exceeding Rs. 200; | Forty paise | |||

| And for every Rs. 200 or part there of secured in excess of Rs. 200; | Forty paise | |||

| b) | When the loan is repayable more than three months but not more than eighteen months from the date

of the instrument— |

|||

| For every sum secured not exceeding Rs. 100; | Sixty paise | |||

| and for every Rs. 10 or part there of secured in excess of Rs. 100; | Sixty paise | |||

| 37 | NOTARIAL ACT, that is to say, any instrument, endorsement , note attestation, certificate or entry not being a protest( note . 43) made or signed by a Notary in the execution of the duties of his office, or by any other person lawfully acting as

a Notary |

Three rupees fifty paise | ||

| 38 | NOTE OR MEMORANDUM sent by

a broker or agent to his principal intimating the purchase or sale on account of such principal– |

|||

| a) | Of any goods exceeding in value twenty rupees | One rupee | ||

| b) | Of any stock or marketable security exceeding in value twenty rupees; | Subject to a maximum of fifty rupees, f ifty paise for every Rs 10, 000/- or part

thereof of the value of the stock or security. |

||

| 39 | NOTE OF PROTEST BY THE MASTER OF A SHIP | Two rupees | ||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| 40 | PARTITION – instrument of [ as defined by section 2 (15 )] | The same duty as a Bottomry Bond (No: 14) for the amount or the market value of the separated share or shares of the property.

N. B. :- the largest share remaining after the property is partitioned ( or if there are two or more shares of equal market value and not smaller than any of the other shares, then one of such equal share) shall be deemed to be that from which the other shares are separated: Provided always that :- a) when an instrument of partition containing an agreement to dived property in severality is executed and a partition is effected in pursuance of such agreement, the duty chargeable upon the instrument effecting such partition shall be reduced by the amount of duty paid in respect of the first instrument but shall not be less than five rupees;

b) where land is held on Revenue settlement for a period not exceeding thirty years and paying the full assessment, the market value for the purpose of duty shall be calculated at twenty-five times the annual revenue;

c) Where a final order for effecting a partition passed by any Revenue Authority or any Civil Court, or an award by an Arbitrator directing a partition is stamped with the stamp required for an instrument of partition in pursuance of such order or award is subsequently executed. The duty on such instrument shall not exceed five rupees. |

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| NOTE:- | Stamp duty has been reduced to 1 % in respect of partition deeds relating to partition of properties among Family members (vide Notification I of G. O. Ms. No: 1128 Revenue ( Regn – I)

Department, dated 13 -6 -2005 w. e. f. 1 – 7- 2005 |

||||

| 41 | PARTNER SHIP — | ||||

| A | Instrument of | ||||

| (a) | Where the capital of the partnership does not exceed Rs.

5, 000/- |

One hundred rupees | |||

| b) | In any other case | Five hundred rupees | |||

| B | Reconstitution of — | ||||

| (a) | Where immovable property contributed as share by a partner or partners remains with the f irm at the time of outgoing in whatever manner by such partner or partners

on reconstitution of such partnership |

Five percent on the market value or the immovable property remaining with the firm | |||

| (b) | Any other case | Rupees five hundred | |||

| C | Dissolution of : – | ||||

| (a) | Where the property which belonged to one partner or partners when the partnership commenced is Distributed or allotted or given to another partner or partners | Five percent on the market value equal to the market value of the property distributed or allotted Given to the partner or partners under the instrument of dissolution in addition tot he duty which would have been chargeable on such dissolution i f such property had not been distributed or

allotted or given; |

|||

| (b) | in any other case | Rupees five hundred | |||

| 42 | POWER OF ATTORNEY as defined by section 2 (21) not being a proxy | ||||

| a) | When executed for the sole purpose of procuring the registration of one

or more documents in relation to a single transaction or for admitting executions of one or more such document; |

Twenty rupees | |||

| b) | When authorising one person or more to act in a single transaction

other than the case mention in classes ( a) |

Twenty rupees | |||

| c) | When authorising not more than five persons to act jointly and

severally in more than one transaction or generally |

Fifty rupees | |||

| d) | When authorising more than f ive but more than ten persons to act jointly and severally in more than

one transaction or generally |

Seventy five rupees | |||

| e) | When given for consideration and authorising the attorney to sell any immovable property; | The same duty as conveyance ( No 20) for a consideration or market value equal to the amount

of the consideration. |

|||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| f) | In any other case:

N. B: the term“ Registration” includes every operation incidental to registration under the Registration Act 1908(Central Act 16 of 1908 ). |

Twenty five rupees for each person authorised | |

| g) | When given for construction or development of , or sale or transf er ( in any manner whatsoever ) of, any immovable property

EXPLANATION For the purpose of this article, more persons than one when belonging to the same firm shall be deemed to be one person. |

Five rupees for every one hundred rupees or part thereof on the market value of the property; | |

| Note:- | Stamp duty has been reduced to

(i) Rs 1000/- when the GPA is given in favour of family member and (ii) to 1% when GPA is given in favour of other than family members Vide G. O. Ms. No 1128, Revenue ( Regn-I) Department, dated `13 -06- 2005 w. e. f. 1 -7 -2005

N. B. : the term “ registration’ includes every operation incidental to registration under Registration Act , 1908 ( central Act 16 of 1908) |

||

| 43 | PROTEST OF BILL OF NOTE, that

is to say any declaration in writing made by a Notary or other person lawfully acting as such attesting the dishonour of a bill of exchange or promissory note. |

Three rupees | |

| 44 | PROTEST BY THE MASTER OF

SHIP, that is to say, any declaration of the particulars of her voyage drawn up by him with a view to the adjustment of losses or the calculation of averages, and every declaration in writing made by him against the charters or the consignees for not loading or unloading the ship, when such declaration is attested or certified by a Notary or other person lawfully acting as such. |

Five rupees. | |

| 45 | RECONVEYANCE OF MORTGAGED PROPERTY:- | ||

| a) | If the consideration for which the property was mortgaged does not exceed Rs. 1000 | The same duty as a conveyance ( No : 20 ) for a consideration or market value equal to the amount of such consideration as setforth in the re- conveyance | |

| b) | In any other case | Fifty rupees | |

| 46 | RELEASE , that is to say , | ||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| A) | Any instrument ( not being such a release as is provided for by section 23 – A) whereby a person renounces a claim upon another person or against any specified

property – |

|||

| a) | Where the amount or value of the claim does not exceed Rs. 1000 | Three rupees for every one hundred rupees or part thereof on the consideration for such release as setforth therein or the market value of the property whichever is higher, over which claim is

relinquished. |

||

| B | Where it exceeds Rs. 1, 000/ – | The Same duty as under the Clause ( a) for the first Rs. 1, 000 and for every Rs. 500 or part thereof in excess of Rs. 1000/- fifteen rupees on the consideration or market value of the property, whichever is higher over

which claim is relinquished. |

||

| B) | Release of benami right | The same duty as a conveyance ( No: 20) for a consideration equal to the value of the property as

set forth in the release . |

||

| C) | Release of right of redemption of a mortgage with possession or of the right to obtain reconveyance of property already conveyed. | The same duty as a conveyance ( No: 20) for the amount of such consideration as set forth

in the release. |

||

| 47 | RESPONDENTIA BOND, that is to say, any instrument securing a loan on the cargo laden or to be laden

on board a ship and making repayment contingent on the arrival of the cargo at the port of destination. |

The same duty as a Bottomry Bond (No: 14) for the mount of the loan secured | ||

| 47- A | SALE as defined in section 54 of the Transfer of property Act 1882 | |||

| a) | In respect of property situated in

any local area comprised in a Municipal Corporation: |

|||

| i) | Where the amount or value of the consideration for such sale as set forth in the instrument or the market value of the property which is the subject matter of the sale whichever is higher , but does not

exceed Rs. 1000 /- |

Four rupees for every one hundred rupees or part thereof. | ||

| ii) | Where it exceeds Rs. 1000/ – | The same duty as under clause (i) for the first Rs. 1000 and for every Rs. 500

or part thereof in excess of Rs. 1000 ; twenty rupees. |

||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| b) | In respect of property situated in any local area comprised in the Selection Grade or in Special Grade

Municipality- |

|||

| i) | Where the amount or value of the consideration for such sale as set forth in the instrument or the market value of the property which is the subject matter of the sale, whichever is higher but does not

exceed Rs. 1000 /- |

Four rupees for every one hundred rupees or part thereof | ||

| ii) | Where it exceeds Rs. 1000 / – | The same duty as under clause (i) for the first Rs. 1000, and for every Rs. 500 or part thereof in

excess of Rs. 1000/- twenty rupees. |

||

| c) | Where the property is situated in any area other than those mentioned in Clauses (a) and (b) – | |||

| i) | Where the amount or value of the consideration for such sale as setforth in the instrument or the property which is the subject matter of the sale, whichever is higher, but

does not exceed Rs. 1000/ – |

Four rupees for every one hundred rupees or part thereof. | ||

| ii) | Where it exceeds Rs. 1000 / – | The same duty as under clause ( i) for the f irst Rs. 1000, and for every Rs 500 or part thereof in excess of Rs. 1000/-

twenty rupees. |

||

| d) | If relating to a multi-unit house or unit or apartment/ f lat / portion of multi-storied building or part of such structure of which the provisions of Andhra Pradesh Apartment (promotion of Construction and Ownership Act,

1987, apply:- |

Four rupees for every one hundred or part thereof on consideration or MV which ever higher. | ||

| Note: 1 | Stamp duty payable on sale deed has been reduced to 4% in all areas of Andhra Pradesh under Article 47 – A of Schedule I-A of Stamp Act vide G. O. Ms. No. 162, Revenue (Regn -I) Department Dt: 30. 03. 2013 | |||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| Note: 2 | Transfer Duty/Transfer of Property Tax (TPT) has been reduced to 1. 5% on sale deeds vide

1.G. O. Ms. No. 226 Panchayat Raj & Rural Development (PTS. I) Department, Dt: 06. 04. 2013 , 2. G. O. Ms. No. 150, Municipal Admn and Urban Development (TC) Department, Dt: 6. 04. 2013, 3. G. O. Ms. No. 151, Municipal Admn and Urban Development (TC) Department, Dt: 6. 04. 2013, 4. G. O. Ms. No. 152, Municipal Admn and Urban Development (TC) Department, Dt: 6. 04. 2013, 5. G. O. Ms. No. 153, Municipal Admn and Urban Development (TC) Department, Dt: 6. 04. 2013. |

|||

|

EXPLANATION- I

An agreement to sell followed by or evidencing delivery of possession of the property agreed to be sold shall be chargeable as a ‘ sale ‘ under this article. Provided that, where subsequently a sale deed is executed in pursuance of an agreement of sale as aforesaid or in pursuance of an agreement referred to in clause (B) of article 6, the stamp duty, i f any, already paid or recovered on the agreement of sale shall be adjusted towards the total duty leviable on the sale deed. |

||||

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| 48 | SECURITY BOND or MORTGAGE

DEED executed by way of security for the due execution of an officer or to account for money or other property received by virtue thereof executed by a surety to secure the due performance of a contract

EXEMPTION Bond other instrument; when executed :-

a) by any person for the purpose of guaranteeing that the local income derived from private subscription to a charitable dispensary or hospital or any other object of public utility, shall not be less than a specified sum per mensem;

b) executed by persons taking advance under the Land improvement loan Act 1883, advance under the Land Improvement Loans Act 1983 ( Central Act 19 of 1983 ) of the Agriculturists Loans Act 1884 ( Central Act 12 of 1884) or by their sureties as security for the repayment of such advances ; c) executed by officers of Government or their sureties to secure the due execution of an office or the due accounting for money or other property received by virtue thereof . |

Three per centum of the value of the security subject to a maximum of rupees one hundred. | ||

| 49 | SETTLEMENT :- | |||

| A | Instrument of ( including a deed of dower |

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| a) | Settlement in favour of a member or members of a family.

EXPLANATION

For the purpose of this Article “ Family “ means father, mother, husband, wife, brother, sister, son daughter, and includes grand- father, grand- mother, grand- child, adoptive father or mothers, adopted son or daughter. |

The same duty as Bottomry Bond ( No: 14 ) for a sum equal to the amount or market value of the property settled as set forth in such settlement;

Provided that where and agreement to settle is stamped with the stamp required for an instrument of settlement and an instrument of settlement in pursuance of such agreement is subsequently executed, the duty on such instrument shall be the duty as mentioned in the Article 6. |

||

| b) | In any other case.

Exemption:

Deed of dower executed on occasion of a marriage between Muslims. |

Six-rupees for every hundred rupees or part thereof of the market value of the property which is the subject matter of settlement. | ||

| B | Revocation of – | The same duty as a Bottomry Bond ( No: 14) for a sum equal to the amount of value of the property concerned as set forth in the instrument of

revocation but not exceeding ninety rupees. |

||

| 50 | SHARE WARRANT to bearer issued under the companies Act 1956 (central Act I of 1956). | One and a half times duty payable on Conveyance (No: 20 ) for a consideration or Market value equal to the nominal amount of the shares

specified in the warrant. |

||

| 51. | SHIPPING – ORDER for or relating

toe the conveyance of goods on board of any vessel. |

Twenty paise. | ||

| 52 | SURRENDER OF LEASE ; | |||

| a) | When duty with which the lease chargeable does not exceed thirty

rupees. |

The duty with such lease is chargeable | ||

| b) | In any other case | Thirty rupees | ||

| 53 | TRANSFER ( whether with or without consideration)- | |||

| a) | Of debentures being marketable securities, whether the debenture is liable to duty or not, except debentures provided for by section 8: | One half of the duty payable on a conveyance (No: 20) for a consideration, or market value equal to

the face amount of the debenture . |

||

| b) | of any interest secured by a bond,

mortgage-deed or policy of insurance — |

| Article No | DESCRIPTION OF INSTRUMENT | PROPER STAMP DUTY |

| i) | If the duty on such bond, mortgaged- deed or policy of insurance does not exceed thirty

rupees. |

The duty with which such bond mortgaged- deed or policy of insurance is

chargeable |

||

| ii) | In any other case | Thirty f ive rupees. | ||

| c) | Of any property under the Administration General Act, 1963,

(Central Act 45 of 1963). |

Thirty rupees. | ||

| d) | Of any trust- property from one trustee to another trustee or from a trustee to a beneficiary.

EXEMPTION Transfer by endorsement — |

Thirty rupees or such smaller amount as may be chargeable under clauses (a) and (b) of the Article | ||

| a) | of a bill of exchange, cheque or promissory note ; | |||

| b) | of a bill of lading, delivery order, warrant for goods, or other mercantile document of | |||

| c) | Of a policy of insurance; | |||

| d) | Of securities of the Central Government. | |||

| 54 | TRANSFER OF LEASE by way of assignment and not by way of under – lease | The same duty as a Conveyance ( No: 20) for a consideration or market value equal to the amount

of the consideration for the transfer. |

||

| 55 | Trust– | |||

| A | Declaration of –of , or concerning any property when made by any writing, not being a will or a declaration as provided in section 2(24). | The same duty as a conveyance ( No: 20) for sum equal to the amount or value of the property concerned, as setforth in the instrument but not

exceeding two hundred rupees. |

||

| B | Revocation of-of, or concerning any property when made by an instrument other than a will. | The same duty as a conveyance ( No: 20) for sum equal to the amount or value of the property concerned, as setforth in the instrument but not exceeding one hundred

rupees. |

||

| 56 | WARRANT FOR GOODS, that us to say, any instrument evidencing the title of any person therein named or his assign, of the holder thereof to the property in any goods lying in or upon any dock, warehouse or wharf, such instrument being signed or certified by or on behalf of the

persons in whose custody such goods may be. |

One rupee fifty paise |

Stamp duty in Hyderabad in 2023

| Area in which the property falls | Stamp duty as a percentage of the registered property value | Registration charge as a percentage of the registered property value | Transfer charge as a percentage of the registered property value |

| Gram panchayat | 5.5% | 2% | None |

| Other areas | 5.5% | 0.5% | 1.5% |

Source: registration.telangana.gov.in

Note: There has been no increase in the rate since July 1, 2022.

See also: All about GHMC property tax

Property registration charge for women in Hyderabad, Telangana

Unlike most cities, where the rates are lower if the property title is being transferred in the name of a woman or under joint ownership where a woman is also a party, the stamp duty rates are uniform for men and women in Telangana. Consequently, women home buyers in Hyderabad pay as much stamp duty as their male counterparts.

See also: All about e panchayat Telangana

Property registration charges in Hyderabad in 2023

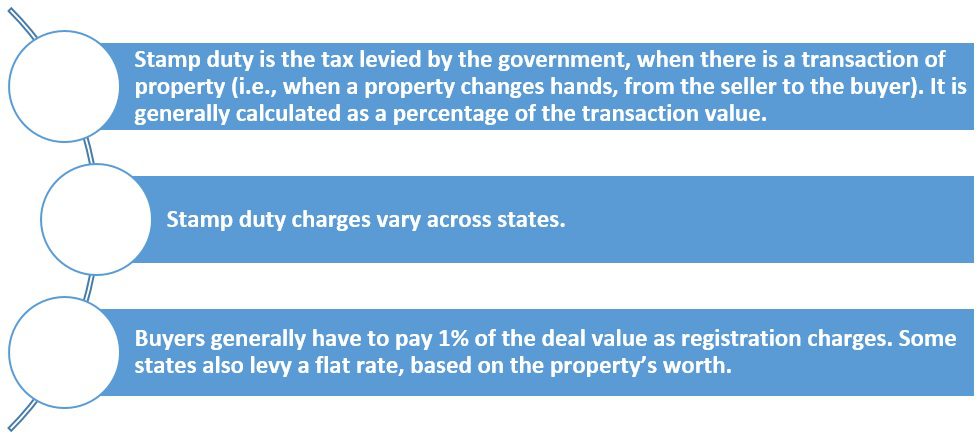

Unlike most states that charge 1% of the deal value as the registration charge, buyers have to pay 2% of the value in Hyderabad. Registration charge is only 0.5% in case the property does not come under a gram panchayat area.

Also read all about Telangana land and property registration

Transfer charge on property purchase in Hyderabad, Telanagana

Apart from stamp duty and registration charges, all buyers also have to pay transfer chargea during property registration in Hyderabad.

Hyderabad stamp duty and registration charge calculation

Suppose Brinda bought a property worth Rs 50 lakh in Hyderabad. She will have to pay 7.5% of the Rs 50 lakh as the stamp duty, registration charge and transfer duty. So, Brinda’s total liability will be:

Total outgo = Rs 3,75,000 lakh

Also read: Cost of living in Hyderabad

What documents are required for property registration in Hyderabad?

Listed below are the documents to be presented at the sub-registrar’s office, to register your Hyderabad property. However, be advised that this list is only indicative and not exhaustive.

The sub-registrar may demand additional documents.

- Original property documents.

- Encumbrance certificate.

- Demand draft / bank challan for stamp duty payment.

- Section 32A photo form of executants and witnesses.

- Identity proof and address proof of the buyer, seller and two witnesses.

- Power of attorney, if applicable.

- Pattadar passbook for agricultural land.

See also: Top localities to invest in Hyderabad

How to pay stamp duty and registration fees in Telangana online?

- Visit the official portal at https://registration.telangana.gov.in/index.htm

- Click on e-stamps under Online Services.

- Upload the relevant documents and pay the requisite fee.

- Book a time slot and appointment with the sub registrar.

- Visit the SRO and get the documents verified. Complete the e-KYC.

- After completing the process, the officer will provide you with an endorsement of the registered document.

How to pay stamp duty and registration fees in Telangana offline?

Visit the sub-registrar’s office with the required documents. Complete the payment of the requisite fee in the form of a challan.

Are tax benefits available on stamp duty and registration charges?

Property buyers can avail on tax benefits for stamp duty payment in Telangana. You can claim a deduction under Section 80C with a maximum deduction amount of Rs 1,50,000.

FAQs

What is the stamp duty for property registration in Hyderabad?

Property buyers have to pay 4% of the property value as stamp duty in Hyderabad.

What is the property registration charge in Hyderabad?

Property buyers have to pay 0.5% of the property value as registration charges in Hyderabad.

| Got any questions or point of view on our article? We would love to hear from you. Write to our Editor-in-Chief Jhumur Ghosh at jhumur.ghosh1@housing.com |