The headwinds of a slower market, combined with demonetisation and RERA, have had an impact on the number of homes launched in Pune, according to the ‘Pune Residential Realty Report for January-June 2017’ by Gera Developments.

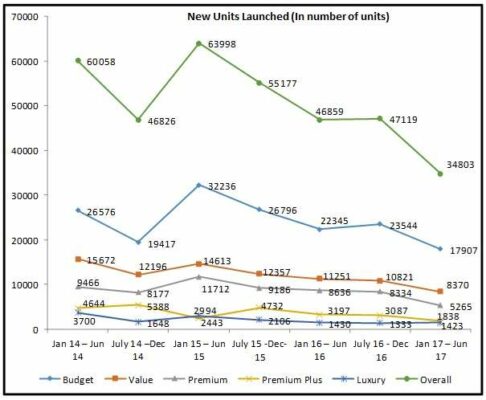

On a year-on-year comparison, 81,922 new homes were launched in the last 12 months (July 2016 to June 2017), down from 1,02,036 homes launched in the previous 12-month period (July 15 to June 16), thereby, a reduction of 19.7 per cent in the total number of flats launched. The last six months alone saw a drop of over 26 per cent in the new homes launched for sale, down from 47,119 flats launched in July-December 2016, to 34,803 flats launched in January-June 2017.

The ‘premium-plus’ segment witnessed a 40 per cent decrease in new flats launched in the last six months, as compared to the previous period. This is followed by a near 37 per cent drop in new units launched in the premium segment. The budget and value segments have not been spared either. Surprisingly, only the luxury segment witnessed a small increase in the number of units launched in the past six months. The average size of flats launched also reduced by 22 per cent over three years, to 722 sq ft, indicating a rising trend of builders moving towards the affordable housing segment.

Pune residential market: Key highlights

- Reduction in new launches: Y-o-Y, the last 12 months has seen a reduction of 19.7 per cent in the total number of flats launched.

- Reduction in sales: There has been a reduction of 16.01 per cent in the offtake from January 2017 to June 2017, as compared to January 2016 to June 2016.

- Sales momentum has moved into the budget and value segments.

- Price trend: Average residential property prices continued to decrease at an overall level, bringing the total drop in property prices since June 2016 to 4.01 per cent in June 2017.

- The PMC area saw a contraction in the market share, from 29.58 per cent, down to 22.09 per cent over the past 30 months.

- The cost of a home of average size at the average price was Rs 58.14 lakhs in June 2014. This cost reduced to Rs 48.83 lakhs in June 2017 – a drop of 16 per cent in three years. Factoring in annual increments over the past three years, affordability of homes is very attractive today.

Commenting on the report, Rohit Gera, managing director of Gera Developments, said: “Never before in the history of India’s real estate industry, have so many industry changing events taken place in such a short period of time. Demonetisation, RERA and GST, have all been introduced in a short period, between November 2016 and July 2017. RERA is a result of the collective misbehavior of a large section of developers. The outcome of this highly regulated, transparent, delivery-oriented law, will be an increase in prices that customers will need to pay for a low-risk environment. The question, however, is when will the demand-supply equation allow for an increase in prices? The changes in measurement (carpet area and proportionate changes for common areas), combined with the new methods for charging for car parking, will render comparison of the pre-RERA pre-GST with the post-RERA post-GST regime as impossible and eventually, a new metric may emerge. The government’s push towards affordable housing seems to be having an impact, with developers launching new residential projects at prices below the average market rate. The share of PMRDA in new launches, has reached an all-time high, clearly indicating that the next wave of development is happening outward. Unsold inventory has decreased, indicating that developers are concentrating on speedy execution of projects. However, offtake has also reduced, as customers and developers adjust to the new regulatory changes. The introduction of the RERA and the GST, will lead to a reduction in the number of projects being launched in the next six months. This will lead to an improvement in the inventory overhang.”

See also: Residential launches decline, as markets gear up to implement RERA: Cushman & Wakefield

Budget home sales in Pune gain momentum

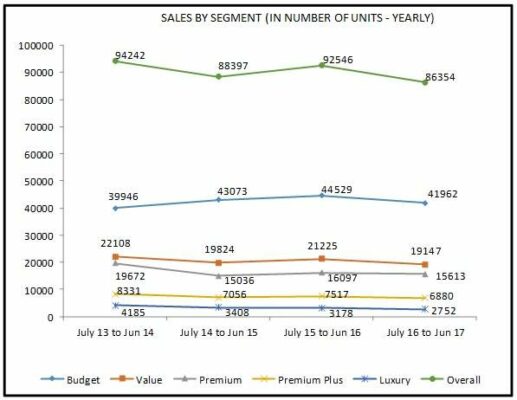

Overall sales have fallen 6.69 per cent, from 92,546 units in July 2015-June 2016 to 86,354 units in July 2016-June 2017. On a half-yearly basis, offtake levels also indicate a stressful situation. Offtake in H1 2016 was 47,704 units, while offtake in H1 2017 was 40,063 units – a drop of 16.01 per cent. The drop in sales is consistent across all sizes. While the total sales have dropped, the market share of the sub-600-sq ft category has increased, with approximately one-fourth of the sales now coming from this segment. Sales momentum has also moved into the budget and value segments. The average size of unsold inventory has steadily reduced from 1,054 sq ft in June 2014 to 940 sq ft in June 2017. The category of houses under 800 sq ft accounted for half of the overall market offtake in Pune.

Property price trends in Pune

The overall average residential property prices continued to decrease, from Rs 4,900 per sq ft in December 2016 to Rs 4,786 per sq ft in June 2017 – a drop of 2.33 per cent, bringing the total drop in property prices since June 2016 (when it was Rs 4,984 per sq ft) to 4.01 per cent. The same trend is seen in new phases of existing projects. New phases were launched at Rs 4,774 per sq ft in H2 2016, as compared to Rs 4,510 per sq ft in H1 2017. The prices in new phases of existing projects were 5.5 per cent lesser in H1 2017, as compared to H2 2015.

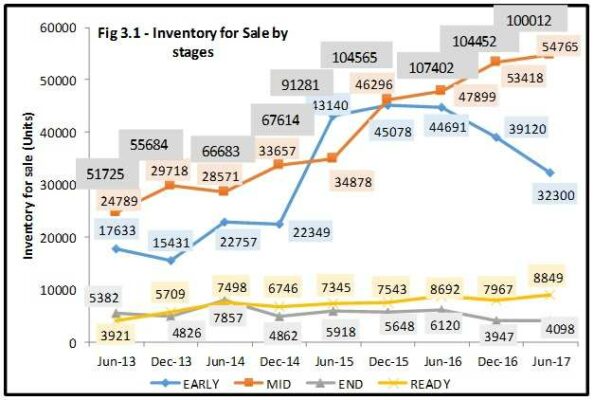

“This indicates that average prices are declining on the whole, but this is on account of new inventory coming in at lower prices and bringing the average down, rather than a correction in existing projects. In real terms, the affordability has increased. Assuming a salary increase of 10 per cent per annum, the same home buyer can afford nearly 35 per cent more now, than they could afford in H2 2013. There is also a lot of talk about home purchases shifting to ready properties, where RERA is not applicable. However, the likelihood of this happening is low for two reasons. First, the inventory of ready homes is very low – while 86,354 units were sold in the last 12 months, there are only 8,849 ready homes available for sale. If demand shifts to ready homes, demand will far outstrip supply, leading to a price rise. Second, if developers are unable to bear the GST costs, they will pass this additional cost on as a price rise” says Gera.

| Location | Price appreciation 24 months |

| Manjari | -21.27% |

| Dhayari | -18.06% |

| Narhe | -16.11% |

| Ambadvet/Mulsi/Tamhini Ghat | -14.40% |

| Warje | -13.00% |

| Aranyeshwar/Balaji Nagar/Bibvewadi/Dhankawadi/Padmavati/Sahakar Nagar/Parvati/Satara Road/Swargate | -10.87% |

| Kondhawe Dhawade /Shivane/Uttam Nagar | -10.15% |

| Bakori/Shirsawadi/Wade Bolhai/Wadegaon | -10.05% |

| Ambegaon | -9.37% |

| Vishrantwadi/Kalas | -7.77% |

Demand and supply of properties in Pune

The gross value of the inventory for sale stood at Rs 49,214 crores, as on June 2017, as against Rs 53,181 crores in Dec 2016, a reduction of 7.46 per cent. This is on account of the reduction in overall inventory for sale and prices over the same period.

The majority of new units launched (from new phases and new projects) have been in the PMRDA region, which accounted for 65 per cent of all new units launched.

When comparing jurisdictions, over the last 24 months, the PMRDA saw a huge increase in its market share from 51.10 per cent to 55.38 per cent. At the same time, the PCMC has retained its share at approximately 21-22 per cent. The PMC area saw a contraction in market share, from 26.42 per cent to 22.09 per cent over the past 24 months. The prices in the PMC region are above Rs 7,000 per sq ft and the slowdown in this segment has affected the PMC areas the most.

Conclusion

As a new paradigm emerges, it is clear that developers will need to be highly compliant, transparent and well capitalised. This will mean that many developers and most fly-by-night operators, will not be able to adhere to the stringent requirements that customers today demand. Hopefully, this will lead to a clean-up of the industry and eventually, change the way the real estate industry is looked at.