Barring agricultural land, one is free to purchase properties in the municipal areas of J&K, even if one is not a domicile of that state. The move follows the withdrawal of J&K’s special status provided under Article 370 of the Constitution on August 5, 2019 and the division of the state into two union territories (UTs) of J&K and Ladakh.

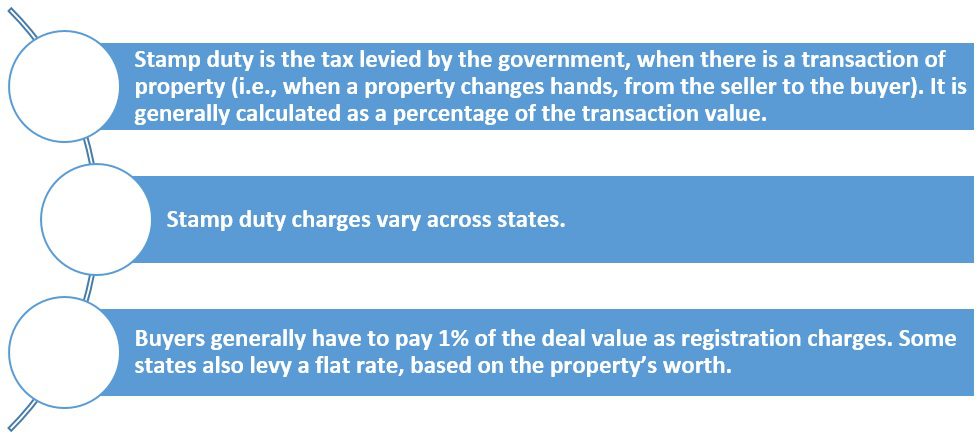

Just like any other Indian state, one is liable to pay stamp duty and registration charges on property purchase to get the asset registered in one’s name. Discussed in this article is the amount you will be paying towards Jammu Kashmir stamp duty and registration charges. Note that the stamp duty and registration charges in Jammu and Kashmir are among the lowest that is charged in India, especially for women.

Stamp duty and registration charges in Jammu and Kashmir in 2024

| Ownership | Stamp duty as percentage of the property value | Registration charge as percentage of the property value |

| Men | 7% | 1.2% |

| Women | 3% | 1.2% |

| Man + man | 7% | 1.2% |

| Man + woman | 5% | 1.2% |

| Woman + woman | 3% | 1.2% |

While 1.2% of the asset value is charged as the registration fee in the UT, this rate is applicable on the registration of sale deeds only. In case the deed type is different, i.e., gift, exchange, relinquishment, etc., the rates vary.

See also: 11 facts about stamp duty levied on property purchase

Stamp duty and registration charges for men in J&K in 2024

In May 2018, former chief minister Mehbooba Mufti abolished the 5% stamp duty that was being charged on the purchase of immovable property by women, providing them a complete waiver of this duty. The move was aimed at encouraging ‘families to register their properties in the names of their sisters, daughters, wives and mothers’. Through the same order the stamp duty charges for men was also reduced to 5% from the earlier 7%. However, following the bifurcation of the state into two UTs in 2019, the stamp duty for women in J&K is 3% of the property value and for men it is 7% of the property value.

| Owner | Stamp duty | Registration fee |

| Man | 7% | 1.2% |

Stamp duty and registration charges for women in J&K in 2024

| Owner | Stamp duty | Registration fee |

| Woman | 3% | 1.2% |

Stamp duty, registration fee on joint ownership in J&K in 2024

| Owner | Stamp duty | Registration fee |

| Man+ Woman | 5% | 1.2% |

| Man+ Man | 7% | 1.2% |

| Woman+ Woman | 5% | 1.2% |

Stamp duty on other deeds in J&K in 2024

| Deed type | Stamp duty | Registration fee |

| Adoption deed | Rs 500 | Rs 2,500 |

| Agreement or Memorandum of an Agreement — (a) If relating to the sale of bill of exchange | One rupee for every Rs 10,000 or part thereof. | Rs 1,000 |

| (b) (i) If relating to the purchase or sale of a [Government of the Union Territory of Jammu and Kashmir] security; | One rupee for every Rs 10,000 or part thereof of the value of the security at the time of its purchase or sale, as the case may be, subject to a maximum of one thousand rupees. | Rs 1,000 |

| (ii) If relating to the purchase or sale of shares, scrips bonds, debentures, debenture-stocks or any other marketable security of a like nature in, or, of any incorporated company or other body corporate. | One rupee for every Rs. 10000 or part thereof of the value of the security at the time of its purchase or sale, as the case may be. | Rs 1,000 |

| (c ) If not otherwise provided for Exemptions:- Agreement or memorandum of an agreement- | One hundred rupees | |

| (a) For or relating to the sale of goods or merchandise exclusively, not being a Note or Memorandum chargeable under article 38; (b) Made in the form of tenderers to the [Government of the Union Territory of Jammu and Kashmir] for, or relating to, any loan. | ||

| Agreement Relating To Deposit Of Title Deeds, Pawn, Pledge Or Hypothecation, that is to say, any instrument evidencing an agreement relating to— | ||

| (a) The deposit of title deeds or instrument constituting or being evidence of the title to any property whatever (other than a marketable security), where such deposit has been made by way of security for the repayment of money, advanced or to be advanced by way of loan or an existing or future debt ; or | 0.25% of the amount secured by such deed, subject to a minimum of Rs 1,000 and a maximum of Rs 50,000. | 0.5% of the value (subject to a minimum of Rs 1,000 and maximum of Rs 5,000) |

| (b) The pawn, pledge or hypothecation of movable property, where such pawn pledge, or hypothecation has been made by way of security for the repayment of money advanced, or to be advanced by way of loan or an existing or future debt— | 0.5% of the value (subject to a minimum of Rs 1,000 and maximum of Rs 5,000) | |

| (i) If such loan or debt is repayable on demand or more than three months from the date of the instrument, evidencing the agreement ; | 0.25% of the amount secured by such deed, subject to a minimum of Rs 1,000 and a maximum of Rs 50,000. | 0.5% of the value (subject to a minimum of Rs 1,000 and maximum of Rs 5,000) |

| (ii) If such loan or debt is repayable not more than three months from the date of such instrument. | Half the duty payable under sub-clause (i) of clause (b) of this article. | 0.5% of the value (subject to a minimum of Rs 1,000 and maximum of Rs 5,000) |

| Explanation :—For the purposes of clause (a) of this article, notwithstanding anything contained in any judgment, decree or order of any court or order of any authority, any letter, note, Memorandum or writing relating to the deposit of title deeds whether written or made either before or at the time when or after the deposit of title deeds is effected, and whether it is in respect of the security for the first loan or any additional loan or loans taken subsequently, such letter, note, memorandum or writing shall, in the absence of any separate agreement or memorandum of agreement relating to deposit of such title deeds, be deemed to be an instrument, evidencing an agreement relating to the deposit of title deeds. | ||

| Exemptions :— | ||

| (a) Letter of hypothecation accompanying a bill of exchange. | — | Rs 1,000 |

| (b) Instrument of pawn or pledge of agriculture produce if unattested. | — | Rs 1,000 |

| Appointment in Execution of a Power, whether of trustees or of property, moveable or immoveable, where made by any writing not being a will. | Rs 100 | Rs 1,000 |

| Appraisement or Valuation, made otherwise than under an order of the court in the course of a suit. | Rs 100 | Rs 1,000 |

| Exemptions:- | ||

| (a) Appraisement or valuation made for the information of one party only, and not veing in any manner obligatory between parties either by agreement or operation of law. (b) Appraisement of crops for the purpose of ascertaining the amount to be given to a landlord as rent. | ||

| BOND, as defined by section 2(5), not being otherwise provided for by any provision of this Act, whether or not relating to particular type of bonds, or by the Court Fees Act | 0.5% of the amount secured by such deed, subject to a maximum of Rs. 5 lakh. | Rs 1,000 |

| Cancellation instrument of, if attested and not otherwise provided for. | 100 | Rs 2,500 |

| Certificate of Sale, (in respect of each property put up as a separate lot and sold), granted to the purchaser of any property sold by public auction by a Civil or Revenue Court or Collector or other Revenue Officer or an officer authorized to do so under any law for the time being in force. | The same duty as a conveyance (No. 18) for a market value equal to the amount of the purchase money only | 1.2% of the value of immovable property |

| Certificate or other Document [except the certificate or other document covered under Articles 22 & 48(A)], evidencing the right or title of the holder thereof, or any other person, either to any shares, scrip or stock in or of any incorporated company or other body corporate, or to become proprietor of shares, scrip or stock in or of any such company or body. | One rupee for every Rs 1,000 or part thereof, the value of shares, scrip or stock subject to minimum of Rs 5. | Rs 1,000 |

| Conveyance, not being a transfer charged or exempted under No. 54 :–– | ||

| a) Where the land or estate is within any urban or rural area | 7% of the market value of such land or area. | 1.2% of the value of the immovable property |

| b) Where the land or estate is within any urban or rural area registered in the name of a female member of the family. | 3% of the market value of such land or area. | 1.2% of the value of the immovable property |

| c) Where the land or estate is within any urban or rural area registered jointly in the name of Husband and Wife. | 5% of the market value of such land or area; Provided that— a) when an instrument relates to an assignment of a debt, the rate of duty applicable shall be 0.5% on the amount of the debt assigned; b) where an agreement to sell an immovable property is stamped with ad valorem duty required for a conveyance and a sale deed in pursuance of such agreement is subsequently executed, the duty on such sale deed shall be the duty payable under the article less the duty already paid, subject to a minimum of Rs. 100; c) where a power of attorney authorising the agent to sell immovable property is stamped with ad valorem duty required for a conveyance and a sale deed is executed in pursuance of power of attorney between the executants of attorney and the person in whose favour it is executed, the duty on the sale deed shall be the duty payable under the article less the duty already paid, subject to a minimum of Rs. 100. d) where a mortgage deed is stamped with ad valorem duty required for a mortgage under article 35 and a court decree in pursuance of a suit filed against the mortgaged property is executed, the duty payable on the decree shall be the duty payable under the article less the duty already paid under article 35 on the mortgage deed, subject to a minimum of Rs. 100. | |

| Explanation:- For the purpose of this article, where in the case of agreement to sell an immovable property, the possession of any immovable property is transferred or agreed to be transferred to the purchaser before the execution or at the time of execution or after the execution of such agreement, then such agreement to sell shall be deemed to be a conveyance and stamp duty thereon shall be levied accordingly: Provided that, the provisions of section 47-A shall apply mutatis mutandis to such agreement which is deemed to be a conveyance as aforesaid, as they apply to a conveyance under that section. | ||

| Exemption:– Assignment of copy right under the Copy Right Act. | ||

| Copy or Extract, certified to be a true copy or extract by or order of any public officer and not chargeable under the law for the time being in force. | Ten rupees. | Rs. 2/- per copy |

| Exemptions :— | ||

| (a) Copy of any paper which a public officer is expressly required by law to make or furnish for record in any public office or for any public purpose ; | ||

| (b) Copy of, or extract from, any register relating to births, baptisms, namings, dedications, marriages, divorces, deaths and burials ; | ||

| (c) Copy of any instrument, the original of which is not chargeable with duty. | ||

| Divorce, Instrument of, that is to say, any instruments by which any person effects the dissolution of his marriage. | Rs 100 | Rs 1,000 |

| Exchange of Property, Instrument of extract certified to be a true copy or extract by or order of any public officer and not chargeable under the law for the time being in force. | The same duty as a conveyance (No.18) on the market value of the property of greater value, which is the subject matter of Exchange. | 1.2% of the value of immovable property |

| Exemptions :– | ||

| (a) Copy of any paper which a public officer is expressly required by law to make or furnish for record in any public office or for any public purpose ; | ||

| (b) Copy of, or extract from, any register relating to births, baptisms, namings, dedications, marriages, divorces, deaths and burials ; | ||

| (c) Copy of any instrument, the original of which is not chargeable with duty. | ||

| Further Change, Instrument of that is to say, any instrument imposing a further charge on mortgaged property– | ||

| (a)when the original mortgage is one of the description referred to in clause(a) of Article No. 35 (that is with possession) ; | The same duty as a conveyance (No. 18) for a market value equal to the amount of further charge secured by such instrument. | 1.2% of the amount of the loan secured. |

| (b) when such mortgage is one of the description referred to in clause (b) of Article No. 35 (that is, without possession)— | ||

| (i) if at the time of the execution of the instrument of further charge, the possession of the property is given or agreed to be given under such instrument ; | The same duty as a conveyance (No. 18) for a market value equal to the total amount of charge (including the original mortgage and any further charge already made) less the duty already paid on such mortgage and further charge. | 1.2% of the amount of the loan secured. |

| (ii) If possession is not so given. | The same duty as a Bond (No. 13) for the amount of the further charge secured by such instrument. | 1.2% of the amount of the loan secured. |

| Gift, Instrument of, not being a settlement (No. 50) or will or transfer (No. 54). | The same duty as a conveyance (No. I8) on the market value of the property, which is the subject matter of the gift. | 0.5% of the value subject to minimum of Rs 1,000 and Maximum of Rs 10,000 |

| Lease, including an under lease, or sub- lease and any agreement to let or sub let or any renewal of lease–– | ||

| (a) whereby such lease, the rent is fixed and no premium is paid or delivered– | ||

| (i) where the lease purports to be for a term less than one year ; | One per cent for the whole amount payable or deliverable under such lease. | 0.1% of the value |

| (ii) where the lease purports to be for a term of not less than one year but not exceeding five years ; | Two per cent for the amount of average annual rent reserved. | 0.1% of the value |

| (iii) where the lease purports to be for a term exceeding ‘‘five years” but not exceeding ten years ;6 | The same duty as a conveyance (No.18) for a market value equal to the amount or value of one and half times the average annual rent reserved. | 0.1% of the value |

| (iv) where the lease purports to be for a term exceeding ten years but not exceeding twenty years ; | The same duty as a conveyance (No. 18) for a market value equal to three times the amount or value of the average annual rent reserved. | 0.1% of the value |

| (v) where the lease purports to be for a term exceeding twenty years but not exceeding thirty years ; | The same duty as a conveyance (No. 18) for a market value equal to five times the amount or value of the average annual rent reserved. | 0.1% of the value |

| (vi) where the lease purports to be for a period in excess of thirty years or in perpetuity or does not purport to be for a definite period ; | The same duty as a conveyance (No. 18) for a market value equal to ten times the amount or value of the average annual rent reserved. | 0.1% of the value |

| (b) when the lease is granted for a fine or premium or money advanced or to be advanced and where no rent is fixed ; | The same duty as a conveyance (No.I8) for a market value equal to the amount or value of such fine or premium or advance as set forth in the lease. | 0.1% of the value |

| (c) where the lease is granted for a fine or premium or money advanced or to be advanced in addition to rent fixed. | The same duty as conveyance (No.I8) for a market value equal to the amount or value of such fine or premium or advance as set forth in the lease, in addition to the duty which would have been payable on such lease, if no fine or premium or advance has been paid or delivered : Provided also that–– (a) when an instrument of agreement to lease is stamped with the ad valorem stamp required for a lease, and a lease in pursuance of such agreement is subsequently executed, the duty on such lease shall not exceed one hundred rupees ; | 0.1% of the value |

| Exemption:-_ Lease and its counterpart executed in case of a cultivator and for the purposes of cultivation (including a lease of trees for the production of food or drink) without the payment or delivery of any fine or premium, when a definite term is expressed and such term does not exceed one year, or when the average annual rent reserved does not exceed one thousand rupees. | 0.1% of the value | |

| (b) where a decree or final order of any Civil Court in respect of a lease is stamped with ad valorem duty required for a lease and an instrument of lease is subsequently executed, the duty on such lease deed shall be the duty payable under the article less, the duty already paid, subject to a minimum of hundred rupees | ||

| Letter of Allotment of Shares, in any company or proposed company or in respect of any loan to be raised by any company or proposed company. | Rates as specified in the Schedule appended to the Indian Stamp Act, 1899 (2 of 1899) | Rs 1,000 |

| Letter of Credit, that is to say, any instrument by which one person authorizes another to give credit to the person in whose favour it is drawn | Ten rupees | Rs 1,000 |

| Letter of Guarantee, that is to say, any instrument by which a person makes him answerable for the debt or default of another | Five hundred rupees | Rs 1,000 |

| Letter of Licence, that is to say, any agreement between a debtor and his creditors that the latter shall for a specified time, suspend their claims and allow the debtor to carry on business at his own discretion. | Five hundred rupees. | Rs 1,000 |

| Memorandum of Association of a Company— | ||

| (a) if accompanied by articles of association under the Companies Act, 1956 (Central Act 1 of 1956); | Rs 500 | Rs 1,000 |

| (b) if not so accompanied | The same duty as is chargeable on Articles of Association under Article 10, according to the share capital of the company. | Rs 1,000 |

| Exemption:– Memorandum of any association not formed for profit and registered under the Companies Act, 1956. | ||

| Mortgage-Deed, not being an agreement relating to the deposit of title deeds, pawn or pledge (No. 6) Mortgage of a crop (No. 36), or a Security Bond (No. 49)- | ||

| (a) when possession of the property or any part of the property comprised in such deed is given by mortgagor or agreed to be given; | The same duty as a conveyance (No.18) for a market value equal to the amount secured by such deed. | 1.2% of the value of loan secured |

| b) when possession is not given or agreed to be given as aforesaid. | 0.5% per cent of the amount secured by such deed, subject to a maximum of ten lakhs. | 1.2% of the value of loan secured |

| Explanation :–A mortgagor who gives to the mortgagee a power of attorney to collect rents of a lease of the property mortgaged or part thereof, is deemed to give possession within the meaning of this article ; | ||

| (c) when a collateral or auxiliary or additional or substituted security, or by way of further assurance for the above mentioned purpose, where the principal or primary security is duly stamped | Five hundred rupees | |

| Mortgage of a crop, including any instrument evidencing an agreement to secure the repayment of a loan made upon any mortgage of a crop, whether the crop is or is not in existence at the time of the mortgage. | Rs 10 | 1.2% of the amount of the loan secured |

| Partition, instrument of. | 2% of the amount of the market value of the separated share or shares of the property. | Rs 1,000 |

| Note :– The largest share remaining after the property is partitioned (or if there are two or more shares of equal value and not smaller than any of the other share, then one of such equal shares) shall be deemed to be that from which the other shares are separated : Provided that— (a) when an instrument of partition containing an agreement to divide property in severalty is executed and a partition is effected in pursuance of such agreement, the duty chargeable upon the instrument effecting such a partition shall be reduced by the amount of duty paid in respect of the first instrument, but shall not be less than one hundred rupees ; (b) where the instrument relates to the partition of agricultural land exclusively, the market value for the purpose of duty shall be calculated at hundred times the annual land revenue ; (c) where a final order for effecting a partition passed by any Revenue- authority or Civil Court or an award by an arbitrator directing a partition, is stamped with the stamp required for an instrument of partition and an instrument of partition in pursuance of such order or award is subsequently executed, the duty on such instrument shall not exceed one hundred rupees. | ||

| Partnership | ||

| A. Instrument of — | ||

| (a) where there is no share of contribution in partnership or where such share of contribution, does not exceed Rs. 50000 ; | Rs 1,000 | Rs 1,000 |

| (b) Where such share of contribution is in excess of Rs. 50000. | Rs 50,000 | Rs 1,000 |

| B. Dissolution of partnership or retirement of a partner or–– | Rs 1,000 | |

| (a) Where on dissolution of partnership or on retirement of a partner, any immovable property is taken as his share by a partner other than a partner who brought in that property as his share of contribution in the partnership ; | The same duty as a conveyance (No. 18) on the market value of such property ; | Rs 1,000 |

| (b) In any other case. | Five hundred rupees. | Rs 1,000 |

| Power of Attorney, [as defined by Section 2(21)], not being a proxy (No. 45)–– | Rs 1,000 | |

| (a) when authorizing one person or more to act in a single transaction, including a power of attorney executed for the sole purpose of procuring the registration of one or more documents in relation to a single transaction or for admitting execution of one or more such documents ; | One hundred rupees. | 0.5% of the value subject to minimum of Rs 1000 and Maximum of Rs 20,000 |

| (b) when authorizing one person to act in more than one transaction or generally, or not more than ten persons to act jointly or severally in more than one transaction or generally ; | One hundred rupees. | 0.5% of the value subject to minimum of Rs 1,000 and Maximum of Rs 20,000 |

| (c) when given for consideration and authorizing the agent to sell any immovable property | The same duty as a conveyance (No. 18) on the market value of the property. | 0.5% of the value subject to minimum of Rs 1,000 and Maximum of Rs 20,000 |

| (d) When given without consideration to a person other than the father, mother, wife or husband, son or daughter, brother or sister in relation to the executants and authorizing such person to sell immovable property situated in Jammu and Kashmir. | The same duty as a conveyance (No. 18) on the market value of the property which is the subject matter of power of attorney. | 0.5% of the value subject to minimum of Rs 1,000 and Maximum of Rs 20,000 |

| (e) in any other case. | One hundred rupees for each person authorized. | 0.5% of the value subject to minimum of Rs 1,000 and Maximum of Rs 20,000 |

| Explanation I:–For the purpose of this article, more persons than one when belonging to the same firm shall be deemed to be one person. | ||

| Explanation II:–The term ‘registration’ includes every operation incidental to registration under the Registration Act, Samvat 1977. | ||

| Reconveyance of Mortaged Property. | Five hundred rupees | Rs 1,000 |

| RELEASE, that is to say, any instrument (not being such a release as is provided for by section 23-A) whereby a person renounces a claim upon another person, or against any specified property. | Two per cent on the market value of the share of the property over which the claim is relinquished, whichever is higher. | Rs 1,000 |

| Security other than Debentures (See Sections 9A and 9B | ||

| (a) Issue of security other than debenture; | .005% | Rs 1,000 |

| (b) Transfer of security other than debenture on delivery basis; | .015% | Rs 1,000 |

| (c) Transfer of security other than debentures on non delivery basis; | .003% | Rs 1,000 |

| (d) Derivatives- | Rs 1,000 | |

| (i) Futures (equity and commodity) | .002% | Rs 1,000 |

| (ii) Options (equity and commodity) | .003% | Rs 1,000 |

| (iii) Currency and interest rate derivatives | .001% | Rs 1,000 |

| (iv) Other derivatives | .002% | Rs 1,000 |

| (e) Government securities | 0% | Rs 1,000 |

| (f) Repo on corporate bonds | .00001% | Rs 1,000 |

| Security Bond Or Mordgage Deed, where such security bond or mortgage deed is executed by way of security for the due execution of an office or to account for money or other property received by virtue thereof, or is executed by a surety to secure the due performance of a contract, or in pursuance of an order of the Court or public officer, not being otherwise provided for by the Court Fees Act. | Five hundred rupees | Rs 1,000 |

| Exemption:- Bond or other instrument, when executed. | ||

| (a) by any person for the purpose of guaranteeing that the local income derived from private subscriptions on a charitable dispensary or hospital or any other object of public utility shall not be less than a specified sum per mensem; | ||

| (b) by persons taking advances under the agriculturist loans or by their sureties as security for the repayment of such advances; | ||

| (c) by officers of the [Government of the Union territory of Jammu and Kashmir] or their sureties to secure the due execution of an office or the due accounting for money or other property received by virtue thereof. | ||

| Settlement– | ||

| A instrutment OF (including a deed of dower). Exemption :– Deed of dower executed on the occasion of or in connection with the marriage between Mohammedans, whether the deed was executed before or after the marriage. | Two per cent of the amount of market value of the property settled : Provided that, where an agreement to settle is stamped with the stamps required for an instrument of settlement and an instrument of settlement in pursuance of such agreement is subsequently executed, the duty on such instrument shall not exceed one hundred rupees. | 0.5% of the value subject to minimum of Rs 1,000 maximum of Rs 10,000 |

| B. Revocation OF. | Five hundred rupees. | Rs 2,500 |

| Surrender of Lease, | Five hundred rupees. | Rs 1000 |

| Explanation :––For the purposes of this article it is immaterial that the surrender of the lease is only as regards the unexpired part of the term, or is with regard to only a portion of the property. | ||

| Exemption :– Surrender of lease, when such lease is exempted from duty. | ||

| Transeer of Lease, by way of assignment and not by way of under lease. | The same duty as a conveyance (No. 18) on the market value of the property which is the subject matter of the transfer | 0.1% of the value |

| Exemption— Transfer of any lease exempt from duty | Explanation-In case of assignment of a mining lease, the market value shall be equal to the amount or value calculated under article 29 depending upon the period of the lease assigned. | |

| Trust–– | ||

| A. Declaration of, or concerning any property when made by any writing not being a will–– | Rs 1000 | |

| (a) where there is disposition of property ; | Two per cent of the market value of the property settled. | Rs 1,000 |

| (b) In any other case. | Five hundred rupees. | Rs 1,000 |

| B. Revocation of, or concerning any property when made by any instrument other than a will. | Five hundred rupees. | Rs 2,500 |

How to calculate stamp duty in Jammu and Kashmir?

- Multiply property value and stamp duty rate. So, for women it will be 3/100 x value of property.

- Next, registration charges will be 1.2% of property value so 1.2/100 x property value.

- Once these are calculated add the stamp duty, registration charges and property value to get total value of property.

Stamp duty calculation in Jammu and Kashmir with example

Here is an example on how to calculate the stamp duty and registration charges, supposing that you purchase a property worth Rs 50 lakh in J&K.

If the property is being registered in the name of a woman:

Stamp duty applicable: 3% of the property value = Rs 1.50 lakh.

Registration charge applicable: 1.2% of the property value = Rs 60,000.

Total stamp duty and registration charge: Rs 2.10 lakh.

If the property is being registered in the name of a man:

Stamp duty applicable: 7% of the property value = Rs 3.50 lakh.

Registration charge applicable: 1.2% of the property value = Rs 60,000.

Total stamp duty and registration charge: Rs 4.10 lakh

If the property is being registered jointly in the names of a woman and a man:

Stamp duty applicable: 5% of the property value = Rs 2.50 lakh

Registration charge applicable: 1.2% of the property value = Rs 60,000.

Total stamp duty and registration charge: Rs 3.10 lakh.

J&K stamp duty calculation in 2024 example with table

| Registry of property value of Rs 50 lakh for different types of buyers | Stamp duty | Registration fee |

| Woman | Rs 1.5 lakh | Rs 60,000 |

| Man | Rs 3.5 lakh | Rs 60,000 |

| Woman + man | Rs 2.5 lakh | Rs 60,000 |

| Woman + woman | Rs 1.5 lakh | Rs 60,000 |

| Man + man | Rs 3.5 lakh | Rs 60,000 |

Rebate on stamp duty for first-time homebuyers in J&K

The Jammu and Kashmir administration in April 2022 approved a 50% remission in stamp duty for those buying residential property for the first time in the Union Territory. The cut will apply on first-time buyers or lessees on purchase or lease of more than 20 years of immovable residential property or apartment or house or a residential plot from any agency of government, or development authority of from developer of project approved by the RERA, the government said in a notification.

Documents to be provided for property registration in J&K

Given below is the list of documents you have to provide, to register a property in J&K:

- Encumbrance certificate

- Challan of stamp duty and registration charge payment

- Proof of identity of the buyer/s and the seller/s

- Details of the property

- PAN card details of both parties

- Power of attorney, if any

- Sale deed

- Map of the land

Note that the list is only indicative and you may be asked to provide additional documents, depending on the type of property you are purchasing.

Property registration in Jammu and Kashmir

You will have to visit the sub-registrar’s office to get the registration done on a pre-scheduled time and date. The state does not offer online property registration services yet.

(Additional Inputs: Anuradha Ramamirtham)

FAQs

Can I buy agricultural land in J&K?

One can buy agricultural land in J&K only after receiving a prior approval from the government. According to the new rules, no sale, gift, exchange or mortgage of any land will be valid, if it is made in favour of a person who is not an agriculturist, unless the government or an officer authorised by the government grants permission for the same.

Can I use agricultural land in J&K for other purposes?

Although agricultural land in J&K cannot be used for non-agricultural purposes, one can do so if they receive the permission of the district collector to do the same.